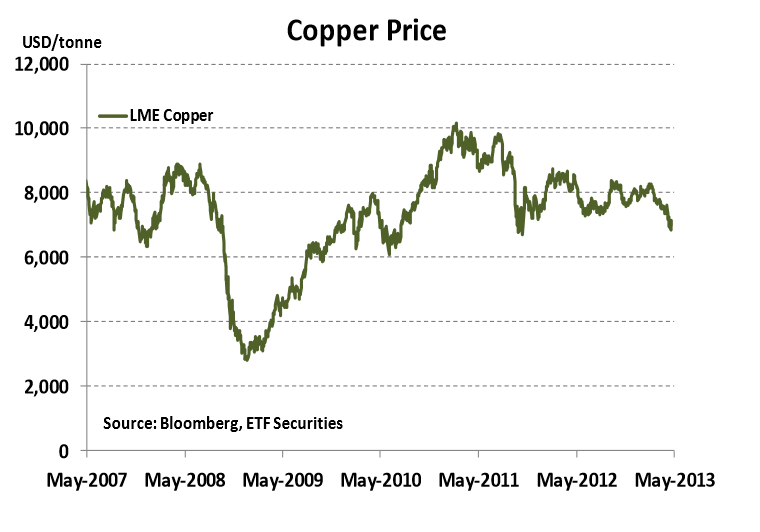

Over the past month, copper prices have reached the lowest level in 18 months, dipping below US$7000 per tonne, as concerns over the robustness of Chinese growth have weighed on the outlook for demand. Early indications of a decoupling from other cyclical assets like equities suggest that fundamentals are playing a larger role in driving prices. In our view, recent negative investor sentiment appears to overstate the bearish case for copper.

Copper is a key input in the industrial production process ranging from power generation to construction to the automotive sector.

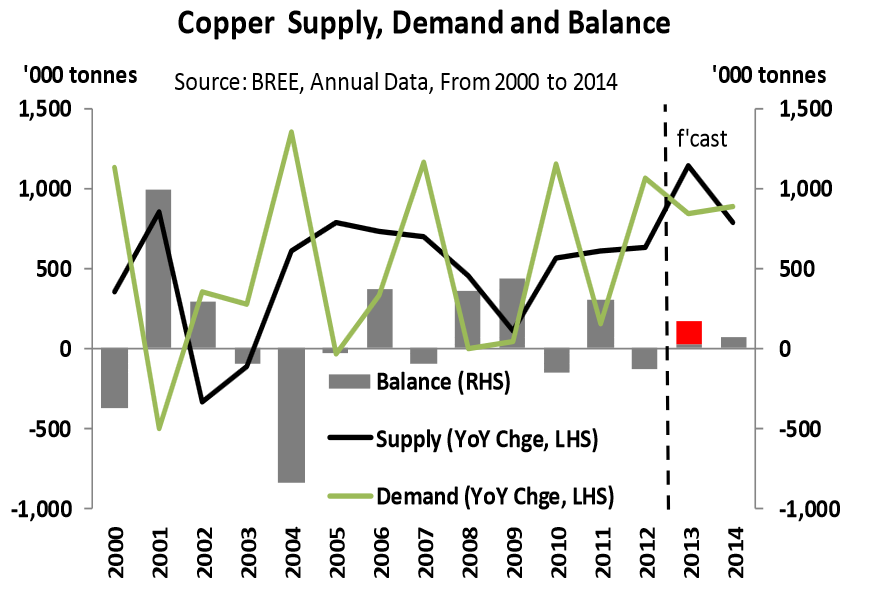

At the beginning of the year, most copper market watchers expected a surplus as rising production outstripped more modest demand growth.

With the global recovery remaining fragile in the face of the recent moderation in growth prospects for the US and China, copper prices looked similarly fragile. However, with central bank stimulus set to stay for the foreseeable future and the supply and demand balance tightening, we contend that the copper market could be at a turning point.

{kind=link}

Next page: Global copper demand

Asia in the Driver’s Seat

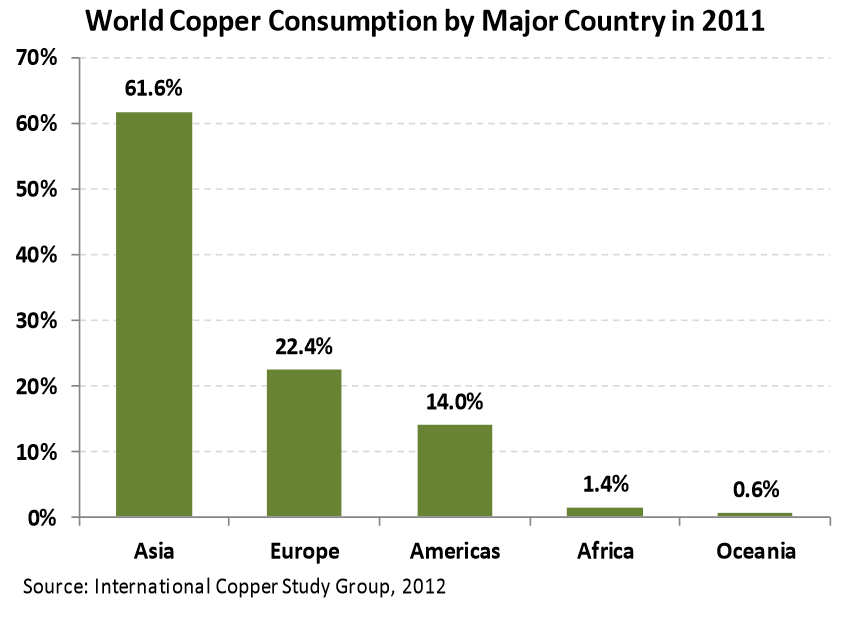

With over 60% of global copper demand deriving from the Asian region (around 40% from China alone), the outlook for growth in the region will remain an important determinant of copper price performance.

{kind=link}

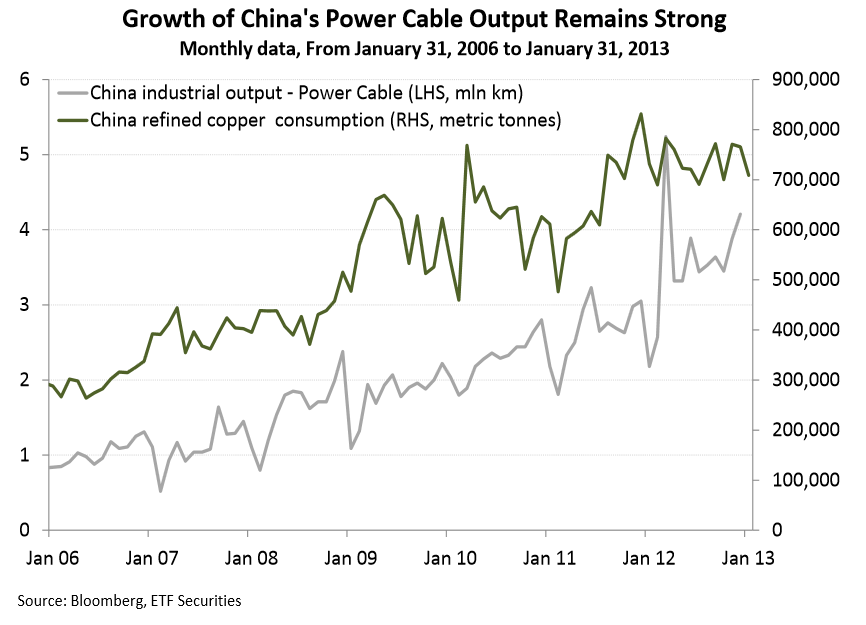

According to Chinese metal research company Antaike, the power sector accounts for over 45% of copper consumption in the country. Industrial output of power cables, a significant source of demand in the power sector, rose by 38% in the 12 months to December 2012.

{kind=link}

From a global perspective, copper benefits from a diversified demand base, with applications ranging from electrical and power generation, to construction, to the auto sector. Overall, one-third of demand comes from electrical applications, another third derives from construction, while another quarter is divided evenly between the transport sector and industrial machinery, according to the Copper Development Association (CDA).

Although Eurozone demand is likely to remain sluggish after a 7% decline in consumption in 2012, the US construction industry, which accounts for nearly half of US copper demand according to the CDA, is likely to continue to improve the demand profile for copper. Housing starts have jumped by 18% over the past 12 months, outpacing the 5% gain in overall US construction spending.

Next page: Copper supply

Tighter Supply

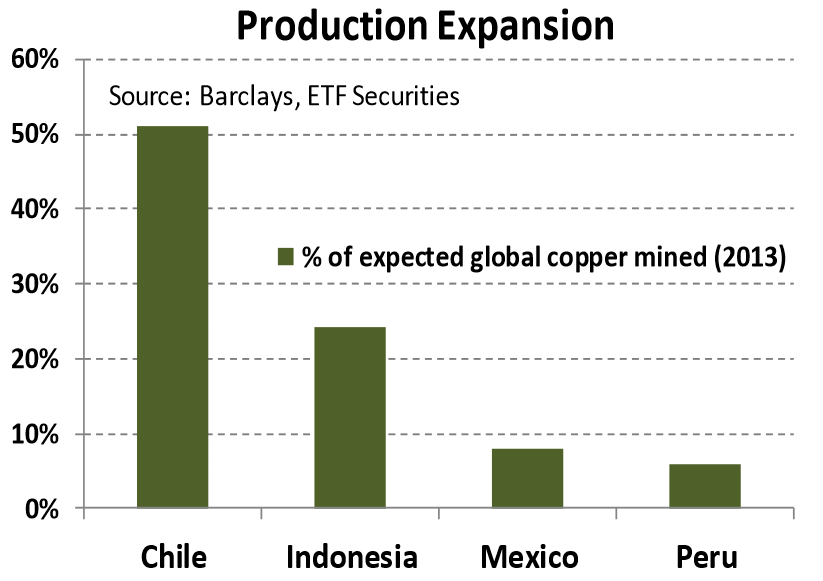

One of the key reasons for weakness in copper prices in the early months of 2013 was expectations that the copper market would return to a surplus in 2013 for the first time in two years. New supply coming on stream from both new and existing mines was expected to outstrip any gains in demand in 2013. Most of the additional supply is expected to come from Chile and Indonesia. Despite potential production expansions, the supply picture is beginning to tighten. Strikes in Chile are an issue that continues to simmer just under the surface. Workers at Codelco, the Chilean state-owned miner and the world’s largest copper producer, staged a one-day strike over job cuts and benefits. While the strike itself did little damage, the potential of a significant supply disruption lingers after the President of the Copper Workers’ Federation suggested that if ‘serious solutions’ are not found, further strikes may occur. The Bureau for Resource and Energy Economics’ (BREE) expectations for 2013 Chilean copper mining growth were just 2% yoy. Such modest growth is likely to shrink if further disruptions to supply, particularly from labour disputes, impact production operations.

{kind=link}

Meanwhile, the recent landslide at Rio Tinto’s Bingham Canyon mine in the US state of Utah has potentially reduced mine production by 50%, according to Kennecott Copper, the mine’s operator. The US is the fourth largest global copper producing country, behind Chile, China and Peru and the mine wall collapse highlights the delicate balance of the copper market in the current environment.

{kind=link}

BREE had, prior to events over the past month, anticipated a copper surplus of around 175k tonnes in 2013. With between 100-150k tonnes taken offline because of the Bingham Canyon event, the surplus expected for 2013 is now threatening to become another deficit.

Next page: Inventory levels

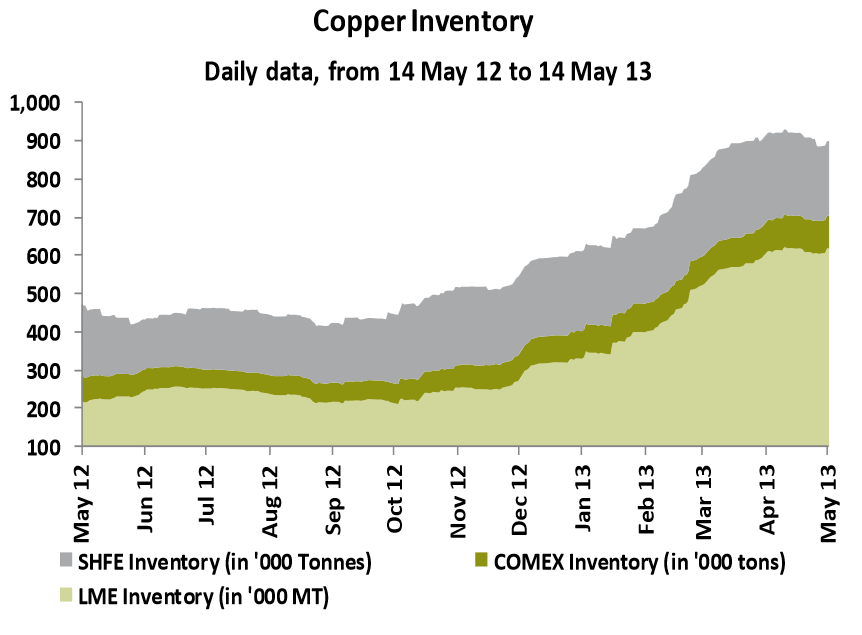

The Bottom Line: Inventories

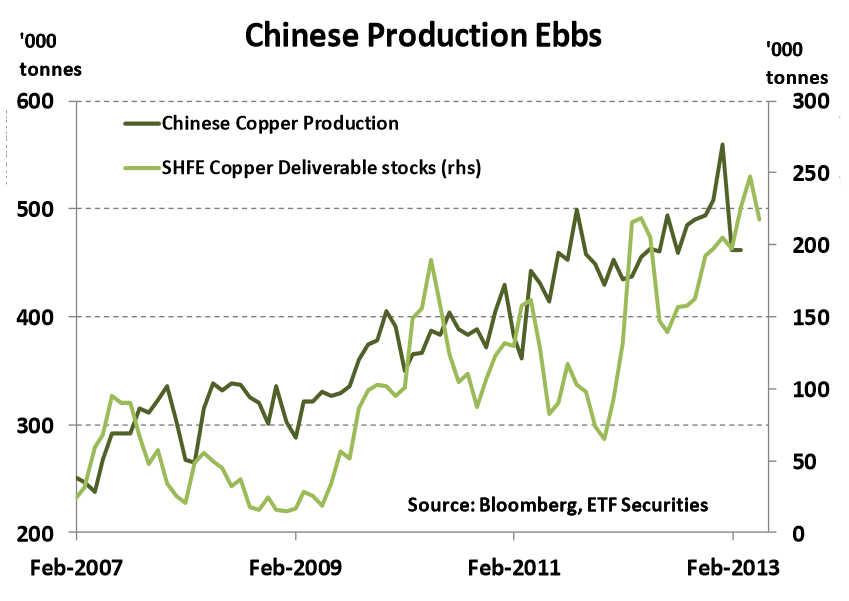

Sluggish growth in recent months has seen global inventory levels climb to the highest levels in 9 years. Stockpiles at LME warehouses have been particularly buoyant. As supply has begun to tighten, however, the trend appears to be reaching a turning point. This is potentially significant as historically prices have reacted more to changes in inventories rather than to the absolute levels of inventories. Chinese stockpiles have fallen by 14% over the past month, as production has been cut back. Historically, Chinese production cuts have occurred when the price of copper on the Shanghai Futures Exchange has been at a premium to the LME price, a situation now in place. China’s imports have been mixed in recent months, with port strikes in Chile likely exacerbating the decline in April copper imports.

{kind=link}

{kind=link}

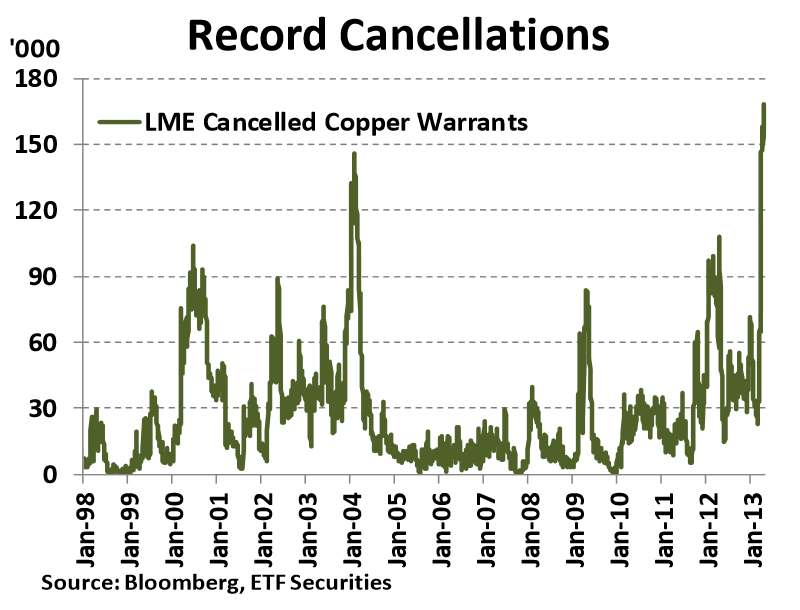

Alongside recent signs of an inventory drawdown have been other indications of rising demand. Warrant cancellations at the LME remain near the record level reached in late April 2013. Cancellations are the amount of tonnage no longer available for trade and give an indication of the amount of metal that is available for removal from warehouses, potentially translating into a reduction in inventory levels.

{kind=link}

Next page: Positioning in copper

How are Investors Positioned?

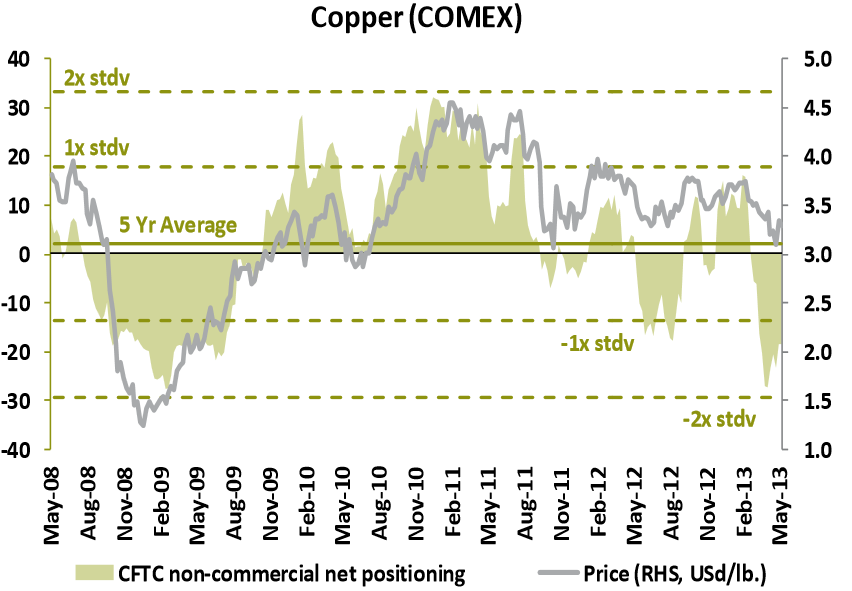

Futures market positioning is the most bearish for copper since early 2009. Net short positions lengthened over the past month and nearly reached two standard deviations from the mean level over the past five years, suggesting an extremely bearish market mindset. With correlations between commodities and other asset classes declining in recent months, fundamentals should continue to determine price direction. Such bearishness appears overdone in our view and with investors positioned aggressively short, any positive news on the fundamental front, could see a sharp short covering rally.

{kind=link}

Conclusion

A sustained move lower in global inventory positioning, supported by rising Chinese imports would indicate strengthening Chinese demand and the beginning of a potential turning point for copper demand. With mine supply uncertainty threatening to push the copper market int o deficit in 2013, the beginning of the stock drawdown could provide a potential entry point to establish long copper positions. The current bearish sentiment toward copper, as reflected in futures market positioning, has the potential to see a sharp move higher fueled by an unwinding of the aggressively short market positioning.