As I’ve mentioned before, although emerging markets have gotten off to a poor start in 2013, I still expect them to outperform developed markets this year thanks to cheaper valuations and more attractive fundamentals, including faster growth.

But while I prefer emerging markets to developed ones, I understand that not all investors are willing to embrace emerging market equities considering the stocks’ underperformance so far this year.

The good news, however, as pointed out in a recent commentary from the BlackRock Global Allocation Team, is that investing directly in emerging markets isn’t the only way to access growth in the emerging world. In fact, because where a company is headquartered doesn’t necessarily indicate where it generates the bulks of its revenues. Investors can access the emerging market consumer through more traditional investments like certain global sector stocks and developed world equities. So which global sectors and developed markets provide the greatest exposure to emerging market economies?

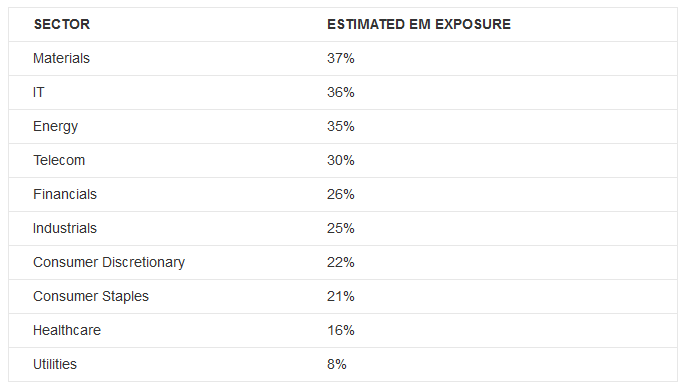

According to an analysis by David Wang, a researcher on my Investment Strategy Group team, materials, energy and information technology have the highest exposure to emerging markets among the 10 global sectors. Meanwhile, Hong Kong, Singapore, and Australia have the highest exposure among the developed markets with the largest market capitalizations (which my team tracks in our monthly Investment Directions commentary).

David determined this ranking by looking at available earnings filings to determine where the companies included in the various S&P Global 1200 sector and MSCI developed world indices generated their revenues. Then, he aggregated that information up to the index level and compared the various indices according to his estimate of what percentage of revenues came from emerging markets. For example, here’s his ranking of how the 10 sectors stack up:

{kind=link}

To be sure, there are some limitations to the analysis. For instance, it’s based on 2011 revenue data since that was what was most widely available. In addition, when companies didn’t disclose the geographic origin of their revenue, he estimated how much came from emerging markets versus developed markets using gross domestic product data.

That said the information can be helpful to investors who want to access emerging market growth through sources other than emerging market stocks themselves. In fact, large exposure to emerging markets is one reason why I currently hold overweight views of the energy and technology sectors, which are accessible through the iShares S&P Global Energy Sector Fund (IXC) and the iShares S&P Global Technology Fund (IXN) respectively.

Russ Koesterich, CFA, is the iShares Global Chief Investment Strategist.

The author is long IXC.