The violence of the fall in the gold price over the past few days has taken investors by surprise and has understandably led to questions about whether this is a short-term correction driven by technical and hedge fund-led speculative activity or if it signals the end of the 12 year gold bull market.

Below we highlight some of the factors behind the recent gold price declines and our view of the longer-term outlook.

• What are the reasons for the downward trend in the gold price since October 2012 and does it represent an end of the 12 year gold price bull market?

The gold price has been trending down since October 2012. The main reason for the fall in the gold price has been rising global growth expectations, particularly in the US, which has lifted interest rate expectations, ratcheted back quantitative easing expectations and boosted investor appetite for cyclical and risky assets. Normally this alone wouldn’t be enough to knock back the gold price, as during most risk-on moves the US dollar weakens which often helps support the gold price. However, because of the dire macro situation in Europe and aggressive quantitative easing by the Bank of Japan, during this risk-on move the US dollar has actually strengthened. This has added further impetus to the downward move in the gold price.

The gold price will face headwinds as long as US interest rate expectations continue to rise and the US dollar continues to strengthen. However, in our view these are tactical/cyclical factors that are temporary. The rise in developed economy debt burdens, driven by demographic change and entrenched interests, continues unabated. Interest rates will need to remain structurally low to offset fiscal drag, keep interest rate payments from ballooning and support growth. Quantitative easing expectations will ebb and flow with business cycle developments.

But until the countries backing the world’s major reserve currencies put in place credible policies to control their growing debt burdens, the public will look to gold as one of the few hard currency hedges against the risk these countries continue to try to reduce their real debt burdens through the debasement of the purchasing power of their currencies. Gold will remain in a bull market until these debt issues are resolved or a credible and liquid alternative to the current fiat reserve currencies emerges.

• What triggered the very sharp sell-off in gold last Friday and Monday of this week?

There were a number of fundamental, technical and investor behavior factors that likely drove the most recent correction in the gold price. In our view it was a classic case of speculative investors taking advantage of gold-negative fundamental news and technical break-points to drive a self-fulfilling downward cascade of the gold price. Given the size of short COMEX futures positions, an equally powerful short-covering rally may also occur once markets have stabilized, new technical levels evolve and gold fundamental news improves. Below we list some of the fundamental and technical factors that may have helped catalyze the most recent frenzy of investor selling.

o The Fed FOMC minutes released on 10th April which showed some members favor an earlier exit from the quantitative easing (QE) than previously assumed.

o Reports that Cyprus was readying the sale of its excess gold reserves to help fund its government’s debt payments led to fears that the gold supply will increase. While Cyprus’ gold stock remains too small to have a material impact on gold prices, investors fear that other troubled European states could follow suit.

o Arguably the most important catalyst was that a number of gold price technical support levels were breached (with some saying they were strategically pushed through by well-timed large hedge fund selling), triggering margin calls, momentum and model-based investor selling. This then created a cascading and self-fulfilling downward spiral in the gold price.

• Is gold in a bubble?

Looking at the past 10 year performance of gold to known historic bubbles in other assets, we can see that price gains in gold have been modest. For example looking at the 10 years running up to the peak of the NASDAQ bubble of 2000 and the gold bubble of 1980, the rise of the gold price seems far from excessive. With gold price at a 2-year low, this could be perceived as a potential buying opportunity. The governments backing the world’s major reserve currencies are faced with extremely large and growing debt burdens. Aging populations and insufficient working population to support current levels of benefits means that debt levels will swell significantly further without very substantial and politically painful cuts or tax raises. These can also be counter-productive to the extent they reduce economic growth and therefore government revenues. This puts government in a particularly tight bind. Europe faces the added problem of backing a single currency for countries with substantially different economic and social fundamentals. Until these issues are resolved there will be a natural demand from the public for alternatives to these fiat currencies. Gold historically has been the first stop of the public when it loses faith that governments will be able to pay back their debts without resorting to inflation/currency debasement. This time is unlikely to be any different.

• What is the outlook for the gold price?

The longer term fundamentals for gold remain strong and ultimately should re-assert themselves once cyclical and technical factors move again in gold’s favor. The fragility of the US recovery, on-going Eurozone weakness and continued high sovereign debt risks are likely to keep central banks firmly in aggressive stimulus mode. The growth of gold supply remains limited with production growing by just over 9% over the past decade and recent disruptions in South Africa threatening miners’ productivity. Emerging market central banks have become large net buyers of gold since 2010, equivalent to around 12% of total supply. Chinese physical demand is the second largest in the world, after India, with Chinese imports of gold now accounting for nearly 20% of total annual demand, from levels of under 3% 10 years ago. China’s demand for gold has been accelerating in recent months.

Given the technical nature of the recent sell-off, short term moves in gold are especially difficult to predict (both up and down). However, at these levels physical buyers – central banks, India and China jewelry demand, long-term strategic investors in gold – will likely start to emerge once the market calms down. Gold needs a positive impetus – a reduction in US interest rate increase expectations, signs of deteriorating European sovereign debt fundamentals, a weaker US dollar – to resume its bull market climb. However, with COMEX speculative short positions at all-time highs, in our view the likelihood of a short-covering rally are now higher than another large downward leg of the price correction.

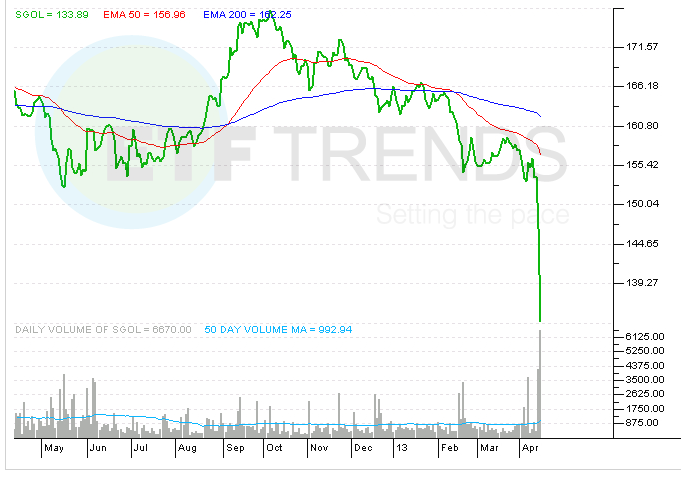

ETFS Physical Swiss Gold Shares (NYSEArca: SGOL)

{kind=link}