• The 6-month cumulative underperformance of defensives: -7.8% (meaning they lagged cyclical stocks by this much)

• The 12-month cumulative underperformance of defensives: -16.1% (meaning they lagged cyclical stocks by this much)

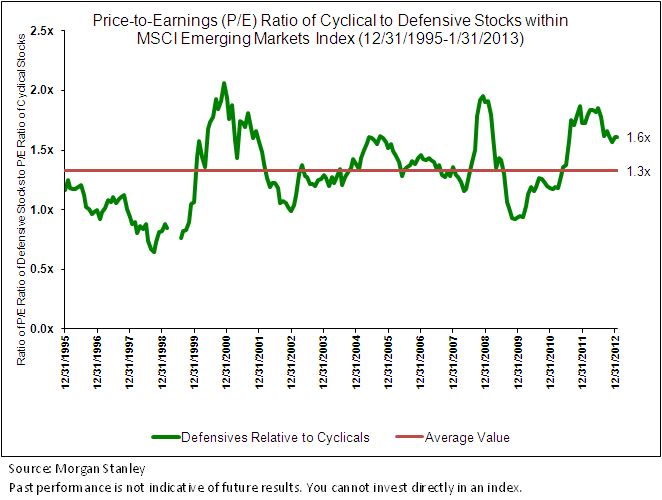

There can be no guarantee that valuations will compress1 or that this relative performance will always hold, but we believe this research to be a powerful illustration encompassing almost 20 years of returns and historical relationships that Morgan Stanley has identified.

WisdomTree’s Current Positioning in Emerging Markets More to Cyclicals

WisdomTree’s Emerging Markets Equity Income Index (WTEMHY) undergoes an annual rules-based rebalance, which is based on a screen run on May 31 of each year. As of the most recent rebalance, based on the May 31, 2012, Index screening, the sectors that saw the highest increases in weight at the rebalance were in the cyclical sectors of Energy and Materials, and sectors that received lower weights at the rebalance were in the defensive basket, namely Consumer Staples and Telecommunication Services.

At no point during the annual screening does WisdomTree’s rebalance process for WTEMHY distinguish between equities that are cyclical and equities that are defensive in nature—the process is purely based on the relationship between dividend growth and price performance over the year leading up to the annual screening date. However, we believe it is worth mentioning WTEMHY’s current positioning—specifically, its over-weight toward two sectors that have underperformed for the most recent full calendar year2.

Conclusion

While there is no way to know future performance with certainty, history has shown a tendency for defensive stocks within the emerging markets to be about 1.3x as expensive as cyclical stocks on a P/E ratio basis. As of January 31, 2013, this figure was over 1.6x, indicating to us that defensive stocks may be expensive in historical terms. While no guarantee of future performance, this makes us supportive of WTEMHY’s current positioning with some of its largest weightings in the Energy and Materials sectors.

{kind=link}

Jeremy Schwartz is director of research at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.

1“Compress” in this context means “become less expensive,” observed through a decline in the P/E ratio.

2Refers to the Energy and Materials sectors within the MSCI Emerging Markets Index for the 2012 calendar year. Source: Bloomberg.