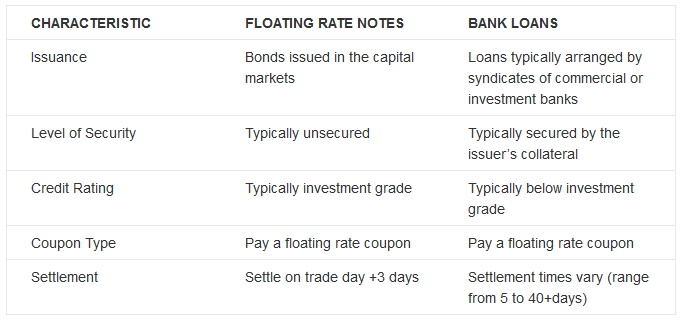

Clients often ask us to explain how FRNs differ from bank loans (sometimes called floating rate loans or leveraged loans). While they share a few similar characteristics, it’s important to understand the differences between them – particularly since most “floating rate” funds are actually bank loan funds. Both instruments pay a coupon that adjusts with changes in short-term rates (primarily 3 month LIBOR), and coupons typically reset on a quarterly basis. The key difference is that FRNs are typically investment grade, whereas most bank loans are rated below investment grade (e.g. high yield). Because of this, bank loans have the potential for higher yield, but of course this comes with greater credit and liquidity risk. Below is a more comprehensive view of the differences between the two securities.

{kind=link}

Bottom line: If you want to insulate a portfolio against interest rate changes, or you want exposure to investment grade bonds with less interest rate risk, floating rate notes may be worth a look. Additionally, FRNs can be a compelling alternative to money market funds if you’re seeking the potential for more yield and you’re willing to take on a bit more risk. Particularly in today’s market environment, where yield is scarce and fears about rising rates abound, FRNs may be the solution you never knew you needed.

Matt Tucker, CFA, is the iShares Head of Fixed Income Strategy.