The ECB, BOE, BOJ, RBA, BOC all had policy meetings last week. While none of them changed interest rates or asset purchases, all indications were for accommodative policy to continue if not become more aggressive.

Meanwhile the data-flow in the US was extremely positive with a large increase in non-farm payrolls (+236k vs. +165k expected) boosting the US dollar. Gold, silver, and platinum fell in dollar terms after the announcement as investors weighed the probability of less easing from the Fed following the recent fall in unemployment to 7.7%, a four-year low.

March will prove to an important month for US fiscal policy, with the need to pass a mini-budget by the 27th to avoid a suspension of government services. Political paralysis remains the key threat to unwinding the recent optimism in the US recovery. With precious metal prices having fallen so much, the cost of insuring against this event looks particularly attractive.

Bargain hunting drives long WTI oil ETCs inflows to largest in 12 weeks, totaling US$11mn. Bargain hunting appears to be driving inflows into WTI crude ETPs, with WTI crude price reaching the lowest level in 2013 last week. Better than expected non-farm payroll numbers on Friday improved the outlook for fuel demand, despite the high level of inventories stored at Cushing, Oklahoma. At the same time, profit taking prompted US$13mn of outflows from natural gas ETCs last week, as prices climbed to a three-month high last week as heavy snow paralyzed the US.

Industrial metal ETPs see largest withdrawal in seven months, on weak Chinese demand. Outflows were concentrated in ETFS Copper (COPA) and ETFS Industrial Metals (AIGI), totaling US$39mn and US$51mn, respectively. Copper imports fell by 15% in February as the Chinese New Year festivity prompted a suspension in economic activity for a week, weighing on industrial metals imports. Weak demand from Europe remains a potential headwind to further rises in copper prices, as the region accounts for 17% of global consumption. However, China is likely to remain a steady source of demand for industrial metals thanks to its planned infrastructure spend.

Gold ETPs experience fifth consecutive weekly outflow, totaling US$150mn. Gold traded in a tight range last week, between US$1,565oz and US$1,585oz, as a stronger US Dollar weighed on gold performance. Despite the on-going exodus from gold ETPs, physical demand from the official sector continues to be supportive with central banks from South Korea to Russia increasing their gold holdings. While gold might need a catalyst to break out of its current tight range, political paralysis from the US to Europe remains a real threat. With the price of gold having declined nearly 5% this year, the cost of insuring against those events looks particularly attractive.

Key events to watch this week: This week, industrial production indices for US, UK and India will be released and will be watched closely to assess the persistence of the global economic recovery. Strong numbers are likely to confirm the improving growth outlook, providing support to more cyclical commodities. US advanced retail sales and University of Michigan confidence index will also be monitored as consumer sector’s strength is fundamental for a full recovery of the US economy.

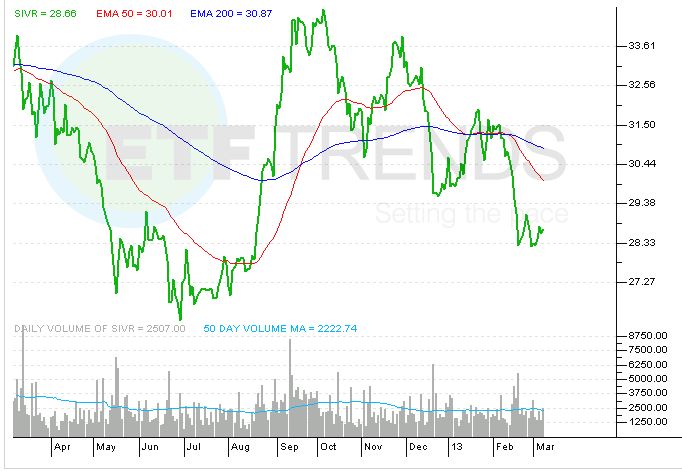

ETFS Physical Silver Shares (NYSEArca: SIVR)

{kind=link}