I have been hearing a lot about rising interest rates. Whether it’s speculation around when the Fed will end quantitative easing and raise the Fed funds rate, or how the 10-year US Treasury yield’s recent rise above 2% may have kicked off a “Great Rotation” from bonds into equities, headlines seem to be sounding the alarm of higher rates.

Take a look at these early year headlines:

- “Ten ETFs to Own if (When) The Fed Raises Rates”

- “Rising Rates Stir Policy Debate”

- “Fed’s Plosser says Long-Term Rates Rose on Economic Outlook”

- “U.S. Rates Will Rise Despite Fed Intervention”

Except, you know what? All of these headlines came out in January or February — but only one of them is from 2013. The first headline is from 2010, the second from 2011, the third 2012, and the last one from this year. Since the beginning of the current post-financial crisis low rate environment, every New Year has started with speculation that this year will be the year that rates finally move higher.

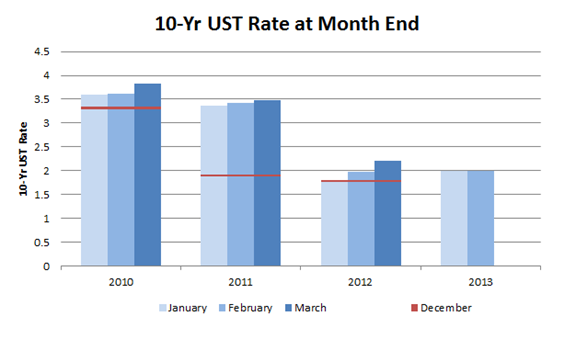

Each year we have seen rates creep higher from January to March, and each year rates have ended December lower then where they started out the year. In fact, the highest rate on the 10-year UST in each calendar year of 2010 – 2012 came in the first few months.

{kind=link}

This pattern raises two questions as we look at the current environment: Why did this trend happen historically? And will it repeat again this year?

I can offer a theory on the first one, and readers of my recent posts can probably guess where I stand on the second.

One potential reason that rising rate concerns surface early in the year could be tied to the eternal optimism that investors seem to feel at the beginning of each year. Economists and investors alike re-set their economic forecasts in January, and they generally have a rosy outlook. Growth will return to normal levels, employment will go up, equities will rise, and yes, bond yields will rise as well. You can see this optimism in equity returns – S&P 500 total returns averaged nearly 8% in the first quarters of 2010, 2011, and 2012. So far this year, it’s up over 8%. As investors compare their strong equity returns to their fixed income returns each Q1, they likely began to express concerns about further rate increases.

Personally I find this timing of expectations resetting to be a bit arbitrary. Markets and economic cycles don’t follow a calendar; there is no reason that the outlook should be significantly different on January 1 than it was on December 1. The 10-year UST does not celebrate New Year’s and isn’t prone to annual bouts of euphoria.

Which brings me to the second question. Despite the turning of the year, the interest rate landscape is largely unchanged. I’ve written before about the three major factors that will likely keep rates low: moderate US growth and inflation, investor demand for US Treasuries to protect against macro risks such as European debt problems, and non-price sensitive UST buyers such as the Fed and other central banks. None of these factors have changed significantly in the first few weeks of this year. This point was reinforced by the recent surprise election in Italy which prompted renewed concern over the European fiscal situation and sent the 10 year UST back down to 1.85%.

Could we see higher 10-year UST rates in December? Of course, but it will require a true shift in economic conditions, and likely a shift in policy by the Fed. Keep an eye on the words and actions of the Fed governors. Based on the most recent FOMC meeting minutes it appears that a healthy debate is emerging about the current QE purchases and their long term impacts. A change in Fed policy and rhetoric is the kind of trigger that could lead to higher interest rates, regardless of the month that it occurs.

Matt Tucker, CFA, is the iShares Head of Fixed Income Strategy.