Historically, one of the more common debates in investing has been the question of whether index or active management is ‘superior.’ Some people get caught up in the idea that one or the other is the better way to go, with lots of data thrown in to support their point.

Others vary their view by market, believing for example that an index mutual fund or ETF is better in efficient markets, while an active fund should be used in inefficient markets.

But many investors and financial professionals – myself included – believe that the answer is not one or the other, but rather both. One has only to look at the investments of pensions, endowments, and other institutional investors to see that the practice of combining index and active is fairly common. And the reason for this is simple: index and active investments have different characteristics, and therefore play different roles in a portfolio.

In fact, blending the two together can help investors meet their objectives better than choosing only one or the other. Active funds aim to produce alpha, or outperformance, but do so by taking on more active risk than index funds. Index funds and index-based ETFs are designed to track a benchmark and, therefore, don’t try to outperform their given market. But they can also help manage overall portfolio risk, are generally low cost and tax efficient, and can provide intraday liquidity.

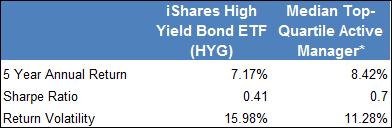

So let’s take a look at an example of how blending active and index can potentially produce a better outcome than just choosing one strategy alone. Below are the risk and return characteristics from the past 5 years for two high yield funds (keep in mind that high yield has historically been a volatile asset class). The first fund is the index-based iShares High Yield Corporate Bond ETF (NYSEArca: HYG) and the second is the median top quartile active manager in the high yield bond space.

{kind=link}

As of 12/31/2012. All performance net of fees.

*The median top-quartile active manager is defined as the manager who achieved the median performance in the top quartile of active managers in the high yield space as of 12/31/2012 (source: Morningstar).

**Return volatility is measured as the standard deviation of monthly returns.

Notice that the active fund has outperformed the index fund and done it with a higher Sharpe ratio (a measure of risk adjusted return) and lower return volatility. At first glance, it would appear that the active fund was the better way to go, and that an index investment may not have a place in this portfolio. But remember – this is assuming that you were able to identify a high-performing active manager (hindsight is always 20/20!). The manager that we picked outperformed 87% of their peers over the 5 year period, whereas the median active manager actually underperformed the index fund during this time period.

Now let’s take a look at a few blended portfolios (below). Notice that within this scenario, a 75/25 active/index mix, you actually get a higher Sharpe ratio than with either the active or index investment on its own. You also reduce risk in the form of return volatility. Your overall return is lower, but you’ve essentially achieved it with less risk. With the blended portfolio, the investor gets the potential for outperformance with the active fund, and the benefits of index – i.e. a way to manage risk and cost while seeking to stay truer to asset allocation goals. For more information about the differences between index and active funds click here.

{kind=link}

As of 12/31/2012.

There is, of course, an important caveat here: no matter what kind of investment you are looking at, the skill of the manager plays a significant role in how well the fund performs after fees, expenses, and tax costs. A skilled index manager will seek to track a benchmark closely, providing returns consistent with an asset class. A skilled active manager will seek to find ways to produce outperformance through different market environments. When evaluating performance for either type of manager, investors have to also consider that taxes can have a significant impact on returns. Before embarking on any portfolio construction exercise, make sure to do your due diligence to help you choose a manager who has the right expertise and track record.

So how should investors think about blending active and index together? Rather than looking at active and index as separate strategies, think about what you need in your portfolio. Can you take on more risk to reach for return? Do you need a way to manage risk in a portfolio? Is intraday liquidity something that you want to have on hand so that you can quickly adjust to future market events? If you start out by asking what you need, you may find that you end up with a surprising answer. Even one that involves an evolved way of thinking: embracing both index and active.

Matt Tucker, CFA, is the iShares Head of Fixed Income Strategy.