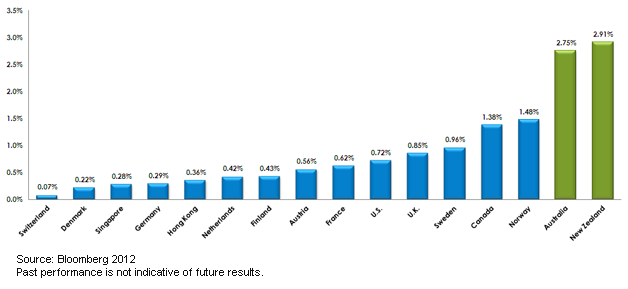

Over the past year, investors continued to look around the world for higher levels of income potential. For some, the decision to allocate to the debt of Australia and New Zealand in 2012 resulted in strong performance compared to U.S. Treasuries.1

But individual investors were not the only market participants looking to diversify their holdings internationally. In fact, central bankers around the world have long allocated a portion of their foreign exchange reserves to Australian assets (such as government bonds).

But in the coming months, the International Monetary Fund (IMF) is expected to publish central bank holdings of the Australian dollar (as well as the Canadian dollar) as part of its official Currency Composition of Official Foreign Exchange Reserves (COFER) database for the first time. This move will add the Australian dollar to the current list of “reserve” currencies: U.S. dollar, euro, British pound, Japanese yen and Swiss franc.

While this doesn’t necessarily create a catalyst for investment, it does validate the perceived strength and stability of Australia’s currency and financial system by global decision makers. Indeed, the term “reserve currency” stems from these government holdings (such as bonds) being held as reserves at central banks around the world.

Taking the interpretation a step further, in the eyes of these government officials, the Australian dollar could increasingly be viewed as a long-term store of value. [Australian Dollar ETF Testing Resistance]

{kind=link}

While Reserve Bank of Australia (RBA) governor Glenn Stevens views the IMF decision as a “classification change,” we believe that increased tracking of the Australian dollar as a reserve currency could pave the way for an increasing allocation in investor portfolios. For 2013, we believe that many of the compelling reasons investors and sovereign wealth funds bought Australian debt in 2012 could continue to provide opportunities in the first half of 2013.

Over the previous calendar year, the WisdomTree Australia & New Zealand Debt Fund (AUNZ) performed well due to a combination of interest rate cuts, higher income potential and positive currency performance against the U.S. dollar. In 2012, the Australian and the New Zealand dollar appreciated against the U.S. dollar by 1.82% and 6.64%, respectively.2

Last September, many market pundits predicted that the Aussie dollar was overvalued, citing continuing concerns about China’s economic outlook. To support economic growth, the RBA cut interest rates by 1.25% over the course of the past year. In the face of these interest rate cuts, the Aussie dollar actually strengthened, a somewhat unexpected result. With better-than-expected economic data continuing to trickle out of China, market sentiment, as well as asset prices, could continue to rise. As ominous clouds surrounding China continue to dissipate, we believe that prospects for the Australian economy could continue to improve along with many other Asian countries.

As the largest market for Australia’s commodity wealth, China was also Australia’s largest overall trading partner in 2011.3 Ultimately, we believe this improvement in the economic outlook could provide a catalyst for a rise in bond prices and investor returns.

Rick Harper is head of fixed income and currency for WisdomTree Asset Management. This post was republished with permission from the WisdomTree blog.

1Sources: WisdomTree, Bloomberg, 2012.

2Source: Bloomberg, 2012

3 Australian Department of Foreign Affairs and Trade, October 2012.