2012 proved a modest year for emerging market (“EM”) currencies, as central bankers from Brasilia to Bangkok attempted to stimulate their economies through interest rate cuts. New asset purchases and policy guidance from the Federal Reserve have had the effect of lowering domestic interest rates and weakening the U.S. dollar compared to most other trading partners and currencies.

On average, EM currencies appreciated in 2012, compared to losses in 2011. However, 2013 may prove to be better than last year, provided such large economies as Brazil, Indonesia and South Africa rebound after currency losses in 2011 and 2012. We believe 2013 will be another year of developed market central bank activism that could provide positive tailwinds for EM currency investors.

After a quick turnaround in risk sentiment in the first few weeks of 2013, investors have done well by having exposure to most emerging market currencies to start the calendar year.

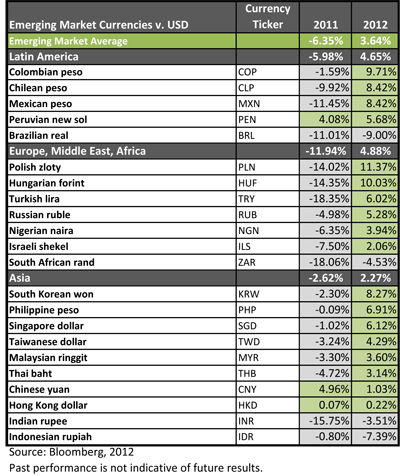

Focusing on 2012, many EM currencies appreciated against the U.S. dollar. Notable laggards included some of the largest emerging market economies, such as Brazil, South Africa and Indonesia. As seen in the table below, broad appreciation was seen in many currencies, but at varying speeds.

On average, investors with exposure to EM currencies were rewarded for taking more risk in 2012. In many instances, currencies that sold off the most in 2011 seemed to rally back at the fastest pace in 2012. Emerging markets in Europe, such as Hungary, rallied strongly after experiencing steep losses in 2011. While concerns about Europe are still in the back of investors’ minds, positive surprises in Europe in 2012 provided a constructive backdrop for currency appreciation in countries such as Poland, Turkey and Russia.

As a region, Asia saw its currencies appreciate at the slowest pace on average. However, a more subdued depreciation in 2011 meant that most Asian currencies have bounced back to levels seen at the end of 2010. Historically, Asian currencies have been less volatile than their Latin American or European counterparts. In uncertain market environments, this has been a benefit for investors. Many economists predict that Asian economies ex-Japan will grow at faster rates in 2013 than Latin America or Europe. Faster growth rates and increased economic output could provide a boost for their currencies in 2013.

Latin American currencies performed well in 2012, with the notable exception of the Brazilian real. After a series of interest rate cuts from 12.50% in September 2011 down to 7.25% in November 2012, the stimulus of the previous year could finally begin to have an effect on the Brazilian economy. Better-than-forecast economic growth could see the Brazilian real appreciate against the U.S. dollar in 2013. In Latin America, another currency poised to continue its upward trend in 2013 could be the Mexican peso. In an environment where the U.S. economy continues to grow at faster rates than developed economies in Europe, Mexico could continue to be a net beneficiary.

While currency movements can be the primary driver of investor returns in non-deliverable forward currency contracts, it is also worth highlighting that even though many emerging market central banks have cut interest rates to stimulate their economies, local interest rates still remain four times higher on average than in the United States. After an active 2012, we believe that the bulk of interest rate cuts in emerging markets have already occurred. For investors in locally denominated debt funds (WisdomTree Emerging Markets Local Debt Fund – ELD or WisdomTree Asia Local Debt Fund – ALD) or EM currency funds (WisdomTree Emerging Currency Fund – CEW)1, we expect returns from currency appreciation and interest income to be more balanced than in 2012.

In light of explicit pledges from developed market central banks to continue accommodative monetary policy, faster-growing economies such as emerging markets could be the net beneficiary in 2013, as investors shift to into higher-yielding, riskier assets. With EM central banks largely on hold, the absence of stimulus from them could remove a potential cause of currency weakness that dampened returns in 2012. For investors that are still underexposed to international currency and fixed income, 2013 could prove to be a great year for gaining exposure to faster-growing economies around the world.

{kind=link}

Rick Harper is head of fixed income and currency for WisdomTree Asset Management. This post was republished with permission from the WisdomTree blog.

1Although CEW invests in very short-term, investment grade instruments, the Fund is not a “money market” Fund and it is not the objective of the Fund to maintain a constant share price.