A prolonged low interest rate environment. An ongoing European debt crisis. An impending fiscal cliff. 2012 presented investors with more than their fair share of challenges, and if we look back at the year’s flows, we can see how investors used fixed income ETFs to navigate the tricky environment.

One big priority for investors this year was income, and investment grade corporate bonds proved to be popular for investors who were on the hunt for yield. Through the end of November, investors had allocated more than $16.1 billion to investment grade credit ETFs. We saw credit spreads on investment grade corporate bonds tighten in by 0.88% to 1.46% over Treasuries1 and total returns were +11.8%2 year-to-date through the end of November.

Credit spreads are a measure of the additional amount of yield the market demands for taking on the credit risk of the issuer. When credit spreads decline, the market is anticipating less concern about credit risk, and bond prices on credit risky bonds generally rise. We saw the iShares $ Investment Grade Corporate Bond Fund (LQD), which celebrated its 10-year anniversary in July, overtake the iShares US TIPS ETF (TIP) as the largest fixed income ETF in the world with over $26 billion in assets under management.

Another big beneficiary of hunt for yield — high yield bond ETFs. These ETFs attracted $10.5 billion as investors were willing to take on more credit risk. Credit spreads on high yield bonds declined by 1.53% to 5.46% over Treasuries3 through the end of November.

US Treasury ETFs experience several flight-to-quality events this year. For instance, after the US presidential election, investors favored longer duration Treasury ETFs to hedge against equity market declines ahead of the fiscal cliff. But overall, these funds had net redemptions of $2.3 billion in 2012. With economic growth remaining slow, inflation became less of a concern among investors and TIP had net redemptions of $559 million over the year. But concern about higher tax rates in 2013 prompted investors to add $3.4 billion to municipal bonds ETFs.

This past year, we observed many investors looking to diversify out of US and developed market investments. To do so, they turned to emerging market debt ETFs. These funds offered compelling yields and less volatility than emerging market equities4. US dollar-denominated EM funds attracted more than $3.6 billion, while local currency (+$1.3 billion) and EM high yield (+$164 million) also gathered assets.

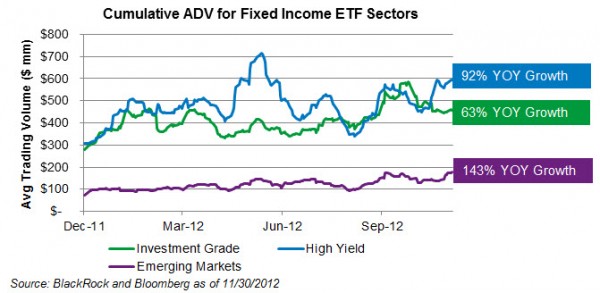

Another trend we observed this year was an increase in liquidity for various segments of the fixed income ETF market. Looking at fixed income ETFs with assets over $1 billion, we can see in this chart below the increase in exchange traded volume as more investors began using the funds.

{kind=link}