When the Federal Reserve met recently, it announced that it would keep the target for its key interest rate near zero until the unemployment rate improves or inflation picks up.

As MarketWatch remarked after the announcement, “Fed policy has now become an open book, as predictable as the tides.”

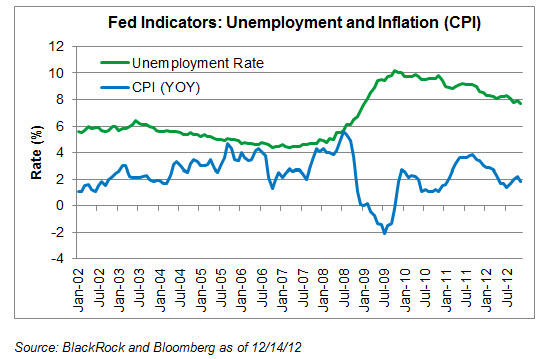

It is true that with these announcements, investors are getting an unprecedented new level of transparency from the Fed. The Fed said it is looking to keep a lid on rates until unemployment, which stands at 7.7%, falls to 6.5% or lower.

This is the first time it has stated an economic target. Since the Fed has a dual mandate for price stability and full employment, it is also watching for inflation to climb up to 2.5% from its current annual rate of 1.8%.

Meanwhile, the Fed is extending its stimulus program, saying it would buy $45 billion in Treasuries and $40 billion in mortgage-backed securities each month.

{kind=link}

At this point, the federal funds rate has been close to zero for four years. But as we head into 2013 and investors look to position portfolios, many are asking whether next year might be the year when interest rates begin to rise. After all, the Fed doesn’t actually set interest rates; rather it tries to influence them through its monetary policy.

Earlier this year, we identified three major factors that were helping to keep a lid on rates:

1.) US economic growth and inflation were holding steady at moderate levels.

2.) There was heightened demand among investors for perceived “safe-haven” investments like US Treasuries given the European debt crisis and larger macro uncertainty.

3.) We continued to see buying of US Treasuries by non-price sensitive buyers such as the Bank of Japan, the Central Bank of China and the Federal Reserve.

As we head into 2013, all three of these forces remain in place. Gross domestic product has grown at a moderate rate of 2.5% year-over-year with inflation readings falling inside the Fed’s target range. Investors continue to look to US Treasuries when markets get rocky (and there are still plenty of rocks out there). And central banks around the world are still active buyers of US government debt.

The most recent announcement helps add clarity to investors’ signposts of rising rates. Because the Fed is explicitly targeting an unemployment level with a limit on inflation, investors now have specific indicators to watch to gauge whether rates may head higher.

Another indication that rates might rise? Less demand for Treasuries, either from central banks or other investors. A reduction in purchases by the Fed or other banks could remove significant buyers from the Treasury market, sending prices lower (and rates higher). Also, if we to see a positive resolution to the ongoing fiscal crisis in Europe and cliff in the US, it could spark increased demand for higher risk assets and a sell-off of US Treasuries. But until any of these events happen, talk of rising rates is likely premature.

The bottom line is that as we head into 2013, we are unlikely to see a significant increase in rates, at least in the near term. The factors that kept interest rates low throughout 2012 appear to be very much in place as the clock ticks down to the New Year.

Matt Tucker, CFA, is the iShares Head of Fixed Income Strategy.