We understand change can be challenging, but it can also mean opportunities.

Take our recent announcement with respect to the adoption of new FTSE benchmark indexes for our international equity mutual funds and exchange traded funds (ETFs). [Vanguard Index Trade ‘All About Costs’]

We believe these indexes offer broad exposure to international markets, and we expect long-term licensing arrangements with FTSE will enable us to deliver considerable expense saving over time.

At the same time, we understand that for some investors this change may be problematic. FTSE classifies South Korea as a developed market, while MSCI classifies it as an emerging market. This means for your developed and emerging markets exposure, you may want to own ETFs that seek to track indexes from either FTSE or MSCI, but not both. If you mix and match, you may own too much South Korea, or none at all.

It’s a dilemma that’s led some investors to reevaluate their holding of Vanguard Emerging Markets Stock Index Fund and ETF (NYSEArca: VWO).

A cost savings opportunity

Herein arises the opportunity. Investors may achieve cost savings by keeping VWO for emerging markets exposure and switching their developed international markets exposure to Vanguard MSCI EAFE (NYSEArca: VEA).

Let’s do the math.

For market-cap-weighted models, broad international stock exposure is gained by allocating about 75% to developed markets and about 25% to emerging markets.

The expense differential in basis points (bps) is clear when we compare our emerging and developed markets ETFs with those iShares ETFs to which they are generally compared. We compare ETFs—not traditional mutual fund shares— because iShares does not have mutual fund shares.

Our emerging markets ETF—the third-largest ETF in the United States, with total assets of $57.4 billion—has a 47 bps advantage over the $37.2 billion iShares MSCI Emerging Markets Index Fund (NYSEArca: EEM). And our $9.3 billion developed markets ETF has a 22 bps advantage over the $36.4 billion iShares MSCI EAFE Index Fund (NYSEArca: EFA). All assets are as of September 30, 2012.

By comparing these ETFs, we are comparing international ETFs that are close in size—they are all among the largest available—and have similar bid/ask spreads. For example, VWO and VEA had average spreads in the third quarter of this year of 0.02% and 0.03%, respectively. EEM and EFA each had an average spread of 0.02%.

There are newer, smaller discount products on the market. But understand that their relatively low trading volume contributes to wider spreads (and potential market impact costs) that may erase any modest expense ratio advantage.

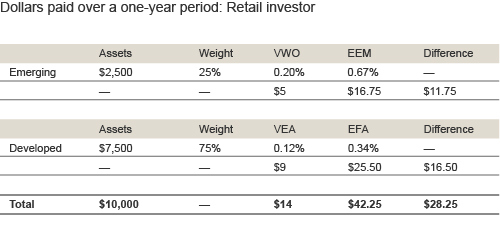

So let’s look at what the differentials mean to a financial advisor and retail investor, in terms of dollars paid over a one-year period. The following examples do not include the brokerage commissions that you may pay to buy and sell ETFs.

Suppose a $10 million international allocation for an advisor, with $7.5 million going to developed markets and $2.5 million to emerging markets.

As you can see in the accompanying table, for every $10 million invested, an investor using Vanguard’s developed markets ETF saves $16,500 and $11,750 using Vanguard’s emerging markets ETF, when compared with the competing iShares ETFs.

Now, look at what a retail investor would pay on a $10,000 international allocation.

{kind=link}

These examples assume that the total annual fund operating expenses remain as stated. The results apply whether or not you redeem your investment at the end of the given period. Your actual costs may be higher or lower.

Financial advisors can get a better idea of the true expense of owning ETFs—whether from Vanguard or another provider—using the cost simulator on our website. Using this tool, advisors can determine the true expense of owning an investment product and its effect on your clients’ portfolios based on factors such as expense ratio, trading costs, and bid-ask spreads.

Accounting for taxes

Then there’s the issue of taxes. Capital losses can be considered an asset in a portfolio when other tax liabilities exist. When an investor’s portfolio has realized gains at year-end, a commonly used strategy is to sell investments at losses (where available) to offset some or all of the expected capital gains.

By switching to VEA from EFA, you could create a loss or a gain depending on when you purchased. The same can be said for potentially moving from VWO to EEM. The decision on taxes—on selling one ETF versus another to harvest losses—is highly unique.

The bottom line: By using a combination of Vanguard ETFs for your developed and emerging markets exposure—ETFs that provide you with broad exposure to international markets—you may achieve savings and have the potential to reduce taxes for your clients.

Notes:

Visit www.vanguard.com to obtain a prospectus for Vanguard and non-Vanguard funds offered through Vanguard Brokerage Services. The prospectus contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

ETF Shares are not redeemable with the issuing Fund other than in Creation Unit aggregations. Instead, investors must buy or sell ETF Shares in the secondary market with the assistance of a stockbroker. In doing so, the investor may incur brokerage commissions and may pay more than net asset value when buying and receive less than net asset value when selling.

All investing is subject to risk, including possible loss of principal. Investments in stocks or bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. Diversification does not ensure a profit or protect against a loss. Stocks of companies based in emerging markets are subject to national and regional political and economic risks and to the risk of currency fluctuations. These risks are especially high in emerging markets.

Fran Kinniry, CFA, is a principal in Vanguard Investment Strategy Group.