If you’ve been following the news this year about exchange traded products (ETPs), you’re already aware that a big theme has been the significant growth the industry has experienced, particularly in the fixed income space.

Bond ETPs are driving industry flows now more than ever, garnering a 30% share year-to-date through September. This growth has driven ETPs to post their strongest year-to-date inflows in history.

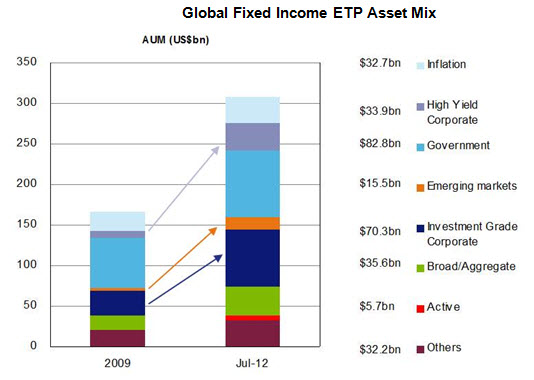

Within the fixed income category, it’s interesting to see how the ETP asset mix has evolved over time – and how it tends to reflect current market and economic conditions. For example, since 2005 we’ve seen a shift from government bond and inflation-related securities (such as Treasury Inflation Protected Securities, or TIPS) to riskier assets like high yield and investment grade corporate bonds (see below).

Given the current low-yield environment, it’s no surprise to see investors being willing to take on more risk in an attempt to reach income objectives. [Emerging Market Bond ETFs for Yield, Diversification]

But what may come as a surprise is the upward trend we’ve seen in emerging market (EM) bond ETP inflows so far this year.

{kind=link}

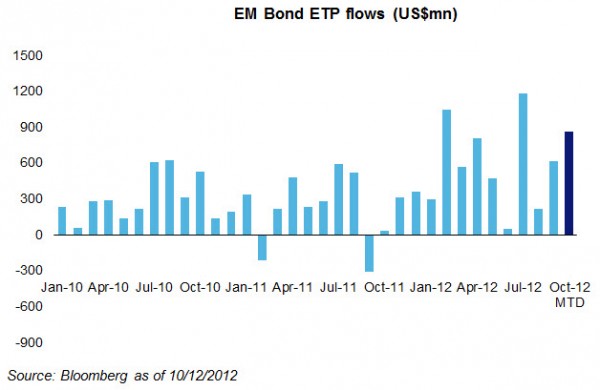

In fact, this has been building for quite a while – as you can see in the chart below, starting in January 2010, inflows for EM bond ETPs have been mostly positive on a monthly basis. The category has taken in over $6bn in net new assets already in 2012 and now accounts for 5% of the fixed income ETP universe, up from less than 2% going into 2010.

{kind=link}

It’s likely that a few factors have contributed to this trend. Clearly there’s been a shift toward riskier assets in general as yield-starved investors strive to meet income objectives. Also, we’ve seen a marked increase in the number and variety of EM bond ETPs available. There are now 57 of these products listed globally, 11 of which were launched this year. Many of the new funds provide increased choice within the category – segments like EM corporate and EM high yield bonds.

And perhaps investors are just getting more comfortable with emerging market bonds. Given that many people look to fixed income for its relative stability, it’s understandable that the shaky governments and economies implied by the term “emerging markets” can be a deal-breaker. However, the problems of the developed world and the slowdown of global growth have begun to cast some of these countries in a new light.

In addition, the characteristics of EM debt have evolved over time. Investors are starting to realize that concerns about volatility and the risks of developing economies may be less than many perceive. For example, 88% of the bonds in the Barclays EM Local Currency Government Index are rated investment grade. Debt-to-GDP ratios are low for many EM countries relative to developed market counterparts. And, EM debt has exhibited low correlations to other asset classes and high historical Sharpe ratios relative to other fixed income segments.

Will we continue to see an upward trend in EM bond ETPs? If the prolonged low interest rate environment persists (and we think it will), we expect to see more investors considering these products as a potential source of yield. In addition, the relatively positive risk/return characteristics and low historical correlations to other segments of the fixed income market should continue to make this category one to watch.

Dodd Kittsley, CFA, is the Head of Global ETP Market Trends Research for BlackRock.