Investors typically don’t like uncertainty, and regulatory uncertainty is no exception. So it’s not surprising that our sales team has been fielding a lot of questions from clients about the iShares S&P US Preferred Stock Index Fund (NYSEArca: PFF).

Clients are wondering what impact regulations put in place after the 2008 financial crisis might have on PFF specifically and preferred securities in general.

As the portfolio manager for our preferred stock ETFs, I spend a lot of time with our sales team and clients, helping them to understand the complexities of these products. Here, I’ve recapped the two main conversations I’ve been having with investors about the effects of these regulations on preferreds:

Q: Will regulatory changes deplete the supply of preferred stocks?

A: First, it’s important to understand what the regulatory changes are, and how they assumedly will affect preferreds. The preferred market is going through a significant transition driven by the Dodd-Frank (D-F) legislation. Under D-F, the Tier 1 capital treatment of hybrid and trust preferreds from bank holding companies will be phased out at 25% per year from 2013 until 2016. The fear is that the law will change the preferred market and could shrink the market size over the next few years. As of 8/4/12 approximately 22% of PFF’s holdings were trust preferreds that would be affected.

So what does this change really mean for preferred stocks? First, it helps to remember that the change does not actually forbid the issuance of trust preferred securities. Even after D-F goes into effect, banks may still choose to issue trust preferred shares, and they can simply opt to exclude them as part of their Tier 1 capital calculation. One reason they may choose to do this is because the interest is tax deductible.

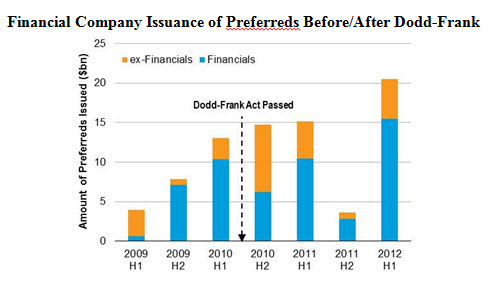

In addition, this change is only aimed at hybrid and trust preferred securities — not the entire asset class. Companies are still issuing and should continue to issue perpetual preferred securities (see chart below). Preferreds are typically a more cost-efficient cost of capital than common equity, and as such they have been an attractive source of financing for companies.

Q:With the onset of the Dodd-Frank Act, will large volumes of preferreds be called?

A: In response to the new rules, banks can either call their preferred securities and replace them with another form of capital if needed, or they can let them continue to mature. The current low rate environment is increasing the possibility of securities of being called similar to any other security that has a call option, and in some cases, banks have the option of calling the securities even prior to normal five-year call protection.

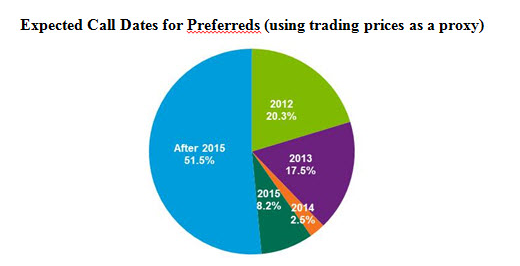

But at this point, we believe it is highly unlikely that banks would call all of their trust preferred securities. Many of them have publicly stated their intention not to – for example, JP Morgan only plans to call half of their trust preferred issues. Instead, we believe banks will call their preferreds over time. While it is always difficult to predict what decisions management will make, we believe the chart below – which illustrates expected call dates for preferreds within PFF if prices remained at current levels and issuers were solely motivated to call based on trading prices – shows a more likely scenario.

The bottom line is that despite these regulatory changes, investors can still consider using preferred stock as part of a diversified income-oriented portfolio. While Dodd-Frank may change the treatment of trust preferred securities, we do not believe it will curtail the supply of preferreds, and as new preferreds are offered, they should continue to make their way in to PFF.

{kind=link}

{kind=link}

Mariela Jobson is Vice President and portfolio manager in BlackRock’s iShares Index Equity Portfolio Management Group.