Despite the negatives, such as the poorer-than-expected jobs numbers and Eurozone risks, U.S. equities, along with stock exchange traded funds, could remain within historical ranges, going into the summer months, says S&P analysts.

Even though the weaker-than-expected jobs report for April “will likely cause this market to endure further choppy action, we don’t see S&P 500 valuations or volatility drifting perilously close to upending extremes,” wrote Sam Stovall, Chief Equity Strategist at S&P Capital IQ, in a research note. [VIX ETFs Sputter as S&P 500 Tries to Break Range]

The trailing 12-month price-to-earnings and earnings yield were holding at the median going back to 1936 of 15.7 and 6.3, respectively.

Additionally, Stovall pointed out that the estimated first quarter year-over-year growth rate of 9.5% is within 1% of the median 8.9% growth rate since the 1930s. He also noted that year-over-year growth will bottom out at 9.0% in the third quarter.

“In other words, the recent deceleration of EPS gains is not necessarily something to be feared, but is reflective of typical reversion to the long-term average,” Stovall said.

However, the analyst also warns investors to take a defensive approach. [An ETF Trend-Following Plan for All Seasons]

“While this ‘median market’ doesn’t look ‘too anything,’ in our opinion, to be sold on its own, trading action will likely remain choppy in the near term, and may again require a retest of the Aril 23 intra-day and closing lows, due to today’s payroll numbers and upcoming French and Greece elections that could unseat those who have already embraced austerity,” Stovall added.

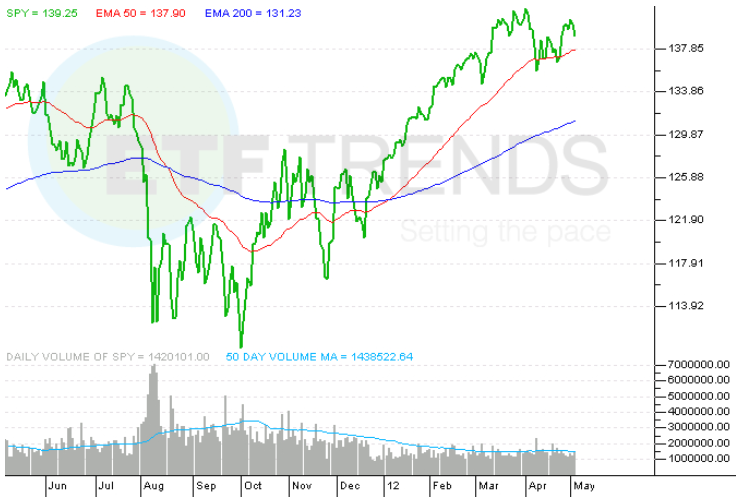

SPDR S&P 500 (NYSEArca: SPY) has gained about 10% year to date.

{kind=link}

For more information on the broad market, visit our S&P 500 category.

Max Chen contributed to this article.

Full disclosure: Tom Lydon’s clients own SPY.