Investors have pumped billions of dollars into high-yield bond ETFs this year, leading some to speculate this new source of inflows has propped up the junk debt market.

However, high-yield mutual funds and ETFs recorded net outflows of about $2.5 billion for the week ended Wednesday, according to reports.

Now, some are wondering about the potential impact if investors start fleeing high-yield ETFs in droves with the same speed they bought the funds.

According to Thomson Reuters-owned Lipper, the past week saw the fourth-largest outflow from junk bond funds since the data provider’s records began in 1992, Dow Jones Newswires reported.

“Big swings in ETFs and mutual funds have many professional investors worried about the potential disruption to prices of their underlying bonds, because big outflows mean that fund managers need to find bonds to sell to meet redemptions,” the newswire said.

Earlier this week, Vanguard said it was closing the $16.9 billion High-Yield Corporate Fund to most new accounts “in an effort to curtain strong cash inflows.” About $2 billion has moved in the door the past six months, the investment manager said. [Vanguard Closes High-Yield Fund — ETF Alternatives]

In the first quarter, Fitch estimates total retail fund flows into high-yield bonds reached $15 billion, with at least 20% of the total resulting from new flows into junk bond ETFs.

In the past week, however, jitters over Greece and the global economy have investors moving away from high-yield bond funds.

The big weekly redemption “seems to represent a snowball effect from transaction in a single ETF,” Reuters reported.

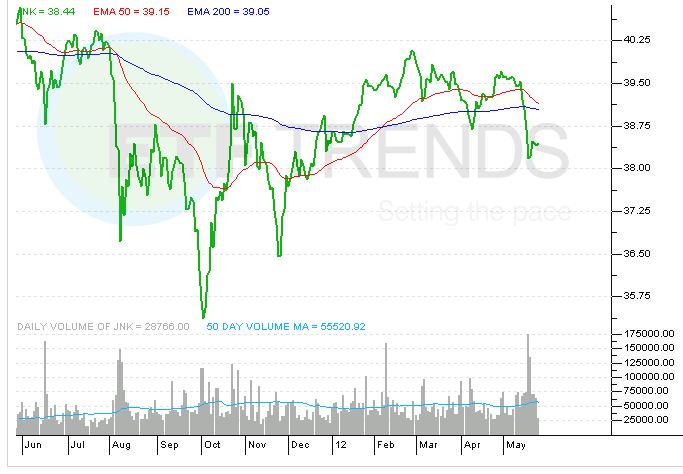

A nearly $800 million trade in SPDR Barclays Capital High Yield Bond (NYSEArca: JNK) has been one of the biggest stories in the ETF business this month. [Will More Big Investors Use ETFs to Disguise Trades?]

JNK reported net outflows of $452 million in the latest week following the prior week’s $871 million net outflow, according to the Reuters article.

“When a large institutional investor took $800 million or so out of a popular junk bond ETF, that may have spooked the retail crowd or tipped off other institutional investors,” said Jeff Tjornehoj, head of Americas Research at Lipper, in the report.

“This in-kind redemption occurred in the data prior to this latest week. However, we are feeling the knock on effect now,” he said.

“Expanded use of high-yield ETFs as a short-term trading platform will likely fuel more market volatility, particularly in periods of macro stress, when risk re-allocation could drive big swings in ETF flows. In periods of asset inflows such as the first quarter, this should support tighter spreads on new issues, particularly for large leveraged issuers whose bonds must be acquired by ETFs,” Fitch said in a separate report.

“At the same time, forced selling could be exacerbated by hot money flows during periods when fundamentals are weakening and investors are pulling back from riskier asset classes,” Fitch added. “This has the potential to reinforce liquidity-driven price moves in high-yield bonds that may have little or no relation to changes in credit fundamentals.”

SPDR Barclays Capital High Yield Bond

{kind=link}