A leveraged volatility ETN was down 18% in Friday’s premarket action following the previous session’s 29% plunge after Credit Suisse said it plans to restart share creation for VelocityShares Daily 2x VIX Short-Term ETN (NYSEArca: TVIX) on a limited basis, causing its premium to collapse further.

The plunge in TVIX shares has been a big market story this week, especially among volatility traders. The ETN had a market cap of $415.4 million after Thursday’s meltdown, so the losses have been considerable in dollar terms.

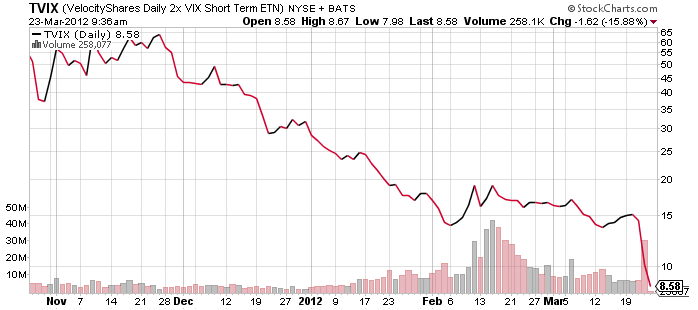

TVIX closed at $10.20 a share on Thursday, while the indicative value stood at $7.83 a share. The ETN was trading hands around $8.40 a share in Friday’s preopen. [Why a Volatility-Linked ETN is Diverging from the VIX]

TVIX is linked to 200% of the daily performance of the S&P 500 VIX Short-Term Futures Index. The note flopped Thursday even though the CBOE Volatility Index, or VIX, rose.

The ETN had been trading at a premium to indicative value after Credit Suisse halted the issuance of further shares due to internal limits on its size. Volatility-linked exchange traded products swelled in assets in early 2012 with many investors apparently positioning for a higher VIX.

ETFs and ETNs have a so-called arbitrage mechanism that generally keeps the price of a share in line with net asset value. However, after TVIX suspended share issuance, it was trading similar to closed-end funds, which can experience premiums and discounts.

Starting Friday, Credit Suisse “may from time to time issue the ETNs into inventory of its affiliates to make the ETNs available for lending at or about rates that prevailed prior to the temporary suspension of issuances of the ETNs,” according to the press release. “Also, beginning as soon as March 28, 2012, Credit Suisse may issue additional ETNs from time to time to be sold solely to authorized market makers.”

Credit Suisse is the issuer for TVIX while VelocityShares markets the ETN.

Credit Suisse’s suspension of new shares caused a supply shortage amid “record demand for volatility products that provide a hedge against U.S. equity losses,” Bloomberg News reported.

Short sellers may have stepped up bets against TVIX on Thursday on speculation TVIX would permit issuance of more shares, according to the report. Trading volume in TVIX jumped to about 30 million shares on Thursday.

“People are likely shorting the TVIX and creating the underlying portfolio by buying the VIX futures to hedge,” Michael McCarty, managing partner at Differential Research, told Bloomberg. “That will cause the premium to contract.”

Volatility exchange traded products are designed to follow VIX futures contracts, rather than the spot price. Adding further complexity, some are ETNs and some are ETFs.

A key difference between the products is that ETNs introduce credit risk because they are debt obligations issued by financial institutions that promise to pay the return of a particular index.

Other exchange traded products designed to rise with VIX futures include iPath S&P 500 VIX Short Term Futures ETN (NYSEArca: VXX) and ProShares Ultra VIX Short Term Futures ETF (NYSEArca: UVXY). They were down fractionally before Friday’s opening bell.

Paul Justice, director of North American ETF research at Morningstar, in a newsletter earlier this month said there was a “fear bubble” in volatility products.

“Irrational exuberance has taken hold in volatility investments. The category gained $1.52 billion in February. Total assets in the category grew by 42% last month and now stand at $3.6 billion,” Justice wrote. “Inflows were so strong that TVIX has suspended new creations. But that hasn’t stopped investors from chasing after it: Investors still demanded it enough to push its price to a … premium over its net asset value.”

He warned: “To me, this is a $3.6 billion disaster waiting to happen.”

Any investors who are using volatility-linked exchange traded products as long-term portfolio hedges are getting hurt by so-called contango in the VIX futures market. [VIX ETFs: Beware Contango]

VelocityShares Daily 2x VIX Short-Term ETN

{kind=link}