Treasury yields have been steadily declining over the past 30 years. Over the next 12 to 24 months, however, yields could begin to rise and investors are about to experience an investment environment that their parents and grandparents can only relate to.

After dropping to historic lows on the so-called risk-off environment during the heightened market volatility witnessed last year, U.S. Treasury yields are beginning to inch higher. As investors become more comfortable with the equities market and take on greater allocations in riskier assets, the long end of the Treasury curve could continue to move upward. Reflecting this trend, Treasury related ETFs have dipped below their key technical support levels.

In this special report on yields we aim to help investors understand that while rising rates may not be one of the most pressing topics de jour, it is still a subject to closely monitor.

- The U.S. Treasuries market has provided investors with a safe and liquid investment, but investors have piled into the asset class, pushing up prices and dampening yields.

- While interest rates will remain at near-zero for now, individuals should be aware of the effects higher yields will play on a fixed-income portfolio. Investors should begin to formulate a strategy to help mitigate the potential hit.

- Lastly, investors relying on the reliability of the money market may soon find themselves scrambling as regulators take a crack at the status quo.

U.S. Treasuries

Treasury ETFs provide the average retail investor with the opportunity to gain a similar investment return to owning the actual Treasury bonds. As such, Treasury ETF investors may enjoy the safe-haven status of the Treasuries market.

For example, during the Eurozone financial debt crisis and downgrade of the U.S. debt last year, Treasury ETFs outperformed as global investors sought the relative safety of the highly liquid U.S. Treasuries market. It is interesting to note that many financial experts largely expected the U.S. large deficit to erode confidence in U.S. assets, especially after the S&P downgraded the country’s sovereign debt from it sterling triple-A status, but investors still fell right back to the comfort of the Treasuries market during any signs of trouble.

Consequently, the flight to quality has pushed yields on long-term Treasuries dated over 20+ years to their mid-2% levels and the benchmark 10-year notes to near all-time lows of around 1.7%. In contrast, 20-year Treasuries over the past decade have provided average yields of 4.7% and 10-year Treasuries showed average yields of 3.7%.

Treasury prices are inversely related to yields. If Treasuries attract greater investment interest, their prices will increase and yields will be pressured. If investors begin to dump Treasuries, prices will fall and yields will begin to rise. We are currently in a three decade long Treasuries market rally as yields on the benchmark 10-year Treasury notes have fallen from over 14% in the early 1980s to below 2% in 2011. Most market observers have argued that Treasury yields are nearing their bottom and the bubble in Treasuries prices will soon burst. [Short ETFs for Rising Interest Rates]

{kind=link}

More recently, the positive market sentiment has lifted investors’ risk profile and sent Treasury investors packing. Treasury prices are falling on the stock markets forward momentum as investors realize that the U.S. economy hasn’t fallen back into a double-dip recession and after the Federal Reserve announced its optimistic economic outlook. Additionally, the financial sector – a major cause for concern in 2008 and the main contributor to the push into safe-haven Treasuries – passed the recent string of stress tests on its large banks. The U.S. economy is adding more jobs, the housing market is slowly improving and consumers are shopping again. So far, all the signs point to optimism.

Investors are beginning to realize that stocks are trading at very cheap valuations, compared to fixed-income assets. Corporations are reporting stronger earnings but their price-to-earnings still remain close to historic averages. Consequently, yields on the benchmark 10-year notes have expanded to recent highs of 2.3% and yields on 30-year Treasuries have hit 3.4%.

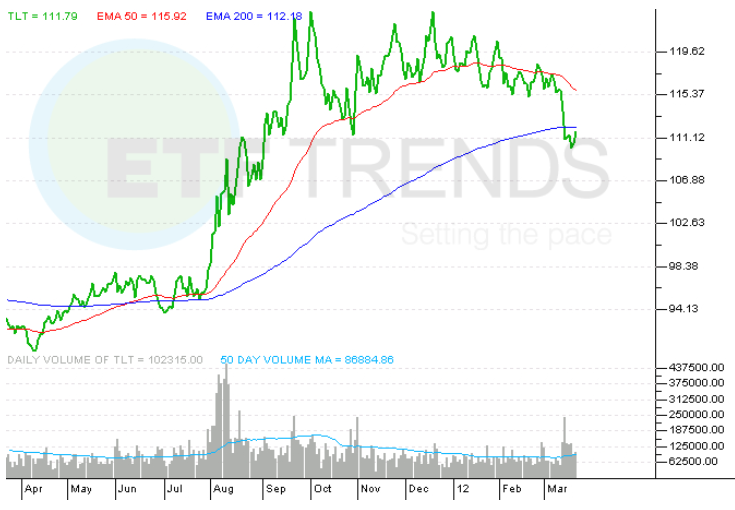

Treasury ETFs, like the iShares Barclays 20 Year Treasury Bond Fund ETF (NYSEArca: TLT) and iShares Barclays 7-10 Year Treasury Bond Fund ETF (NYSEArca: IEF), have fallen below their 50-day exponential moving averages and are now testing their 200-day EMA support level.

iShares Barclays 7-10 Year Treasury Bond Fund ETF

{kind=link}

iShares Barclays 20 Year Treasury Bond Fund ETF

{kind=link}

Interest Rates

The Federal Fund rate can be manipulated as the Federal Reserve supplies more short-term securities in the open market. As the Fed sells the short-term securities, borrowers exchange U.S. dollars for the securities, diminishing the overall money in circulation. Consequently, the less money sloshing around the market raises the short-term interest rates since less credit for borrowers will raise the costs to borrow. As the low-end of the Treasury curve is raised, yields on other Treasuries will begin to follow suit.

{kind=link}

According to a recent paper, authored by Charles Evans, president of the Chicago Fed, and three other economists, the markets are closely scrutinizing Federal Open Market Committee observations and minutes. The research paper reveals that the Federal Reserve’s verbal comments affect the direction in the higher end of the futures curve.

The FOMC’s forecasts on rate paths can influence the direction of yields on later-dated Treasuries if they promise to tightly control shorter term rates. Ever since the financial crisis of 2008, forward guidance on monetary policy statements have been making a greater impact on yields in the Treasuries and corporate bonds markets.

Investors heavily invested in Treasuries or monitoring Treasury yields are ultimately moving on the whims of the Federal Reserve. The Fed will dictate the direction of interest rates and it can artificially lower yields through quantitative easing measures if it feels the economy is not up to par. As the saying goes, “you can’t fight the Fed.”

The Treasury Yield Curve

The Treasury yield curve is the first to move and sets the tone in all domestic interest rates. Interest rates on all bond categories would fall in line and either rise or fall alongside Treasuries.

Investors may notice that the yields on Treasuries is higher on bonds with longer-dated maturities. In an attempt to attract potential investors, bonds or any debt-related security would have to adequately compensate an investor for holding the security over an extended period of time because of the greater risks involved – we might be able to guess what could happen over the next month or two, but we can’t possibly tell what is exactly going to happen in 30 years.

Typically, the yield curve exhibits a concave shape with higher yields as the maturity date pushes outward. The Federal Reserve directly handles short-term interest rates on the lower end of the curve, usually through the federal funds rate, or overnight rate. Later-dated Treasury yields will be determined by the invisible hand on the open markets.

Furthermore, since the yield reflects the nominal interest rate, inflation will diminish the value of the Treasuries. Consequently, the real interest rate, or return after deducting inflation, will be lower in a high inflationary environment. Considering the Federal Reserves loose monetary policies and quantitative easing programs, it is safe to assume that inflation will inevitably surge higher over the next few years and Treasury fund investors should always keep in mind the potential pitfalls of inflation.

The Trend-Following Strategy

{kind=link}

Over time, securities will follow a general trend, and these trends are typically identifiable. The idea is to be fully invested into a certain are when the market is above the long-term trend line, or the 200-day moving average, or look for the exits when the market has dipped below the trend.

Money Markets

{kind=link}

However, after the high volatility witnessed within the markets following the financial crisis, the SEC has begun looking into ways to minimize potential losses in any future financial upheavals. The financial crisis escalated to a new level of uncertainty after the oldest money market fund dipped below $1 a share following the collapse of the Lehman Brothers. Consequently, regulators are proposing to lessen their regulatory grip on the market and let money market funds fall in to a “floating” net asset value and scrapping the money funds’ $1 NAV. Additionally, the SEC is also considering a limit to the the rate of withdrawals investors can make from money market funds. The government contends that the current money-market fund industry, along with the short-term credit market, is not operating under a type of safety net.

If the “floating” rate proposal comes into effect, investors will no longer be able to rely on the money markets as they are known for. Once the floating NAV comes into effect, demand for the products will drop, breaking the buck so to speak. The share prices would be able to fall below the $1 threshold. Chief financial officers and corporate treasurers would find these considerably less appealing if the new rules come into effect as a free floating rule would allow yields on money funds to fall in an already low interest-rate market environment. Additionally, current rules help provide a level of certainty to the market, and some argue that allow the NAV of a money fund to float will cause large investors to lose confidence in the market and stay away from investing in money markets all together.

On the other hand, if federal regulators are also thinking about forcing firms to set aside capital reserves. Investors who want to liquidate all of their holdings will only be able to get around 95% of their money back and wait 30 days before receiving the last 5%. Needless to say, investors will not enjoy the prospect of limited access to their own money.

In either case, any structural changes or tighter regulations may diminish the already low returns on a very large market.