The CBOE Volatility Index or VIX, known as Wall Street’s fear gauge, was up about 10% on Friday afternoon as stocks pulled back on the latest Greece worries.

In the past few sessions, we have observed the VIX creeping higher even though equity indices are also registering new recent highs.

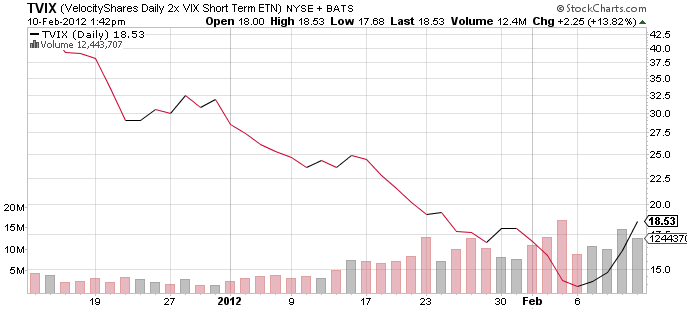

The VIX rose above 20 after closing at 18.63 yesterday and trading as low as 16.10 last Friday.

We noted just last weekend in our weekly recap that “long” VIX exchange traded products such as VelocityShares Daily 2X VIX Short Term ETN (NYSEArca: TVIX) have seen incredible trading volumes recently, and on that note, asset inflows into TVIX most notably late last week and early this week have also been considerable (about 15% of the assets outstanding in the fund have flowed in recently).

Similarly, we started to see call buyers in VIX options late last week as well as earlier this week. This, coupled with the fact that short interest in VIX futures is at its highest levels since 2007, has likely attracted some contrarians to the recent equity rally, whom are taking the “other side” and purchasing “long” VIX products such as TVIX or iPath S&P 500 VIX Short Term Futures ETN (NYSEArca: VXX) as potential portfolio and volatility hedges and/or bearish speculators.

VIX futures have been mired in contango for some time, where distant month futures are priced higher than front month futures and thus the “roll” effect when the funds rebalance their futures upon expiration results in damaging losses for the funds tied to the VIX and rebalanced in this fashion.

However, we note that in the past two sessions, TVIX and VXX alike have demonstrated returns that express “backwardation” in the VIX futures market, which is the opposite state of contango (distant month futures are priced lower than current month futures), and this works to the benefit of “long” VIX products in terms of their performance via tracking the VIX (example, yesterday the VIX was up 2.59%, but TVIX, which is designed to deliver 2 times the daily returns of the index, was up a massive 10%).

Since the “Volatility” space has been an area of significant growth in the ETF/ETN market in the past several years, there is no shortage of products for the portfolio manager to choose from. However, one must be cognizant of the individual index construction methodologies that each product has, along with nuances in regards to leverage and the rebalancing schedule (monthly “roll” or otherwise), and also must closely monitor the VIX spot and futures markets themselves while understanding the positive and negative effects of contango and backwardation.

VelocityShares Daily 2X VIX Short Term ETN

For more information on Street One ETF research and ETF trade execution/liquidity services, contact pweisbruch@streetonefinancial.com.

{kind=link}