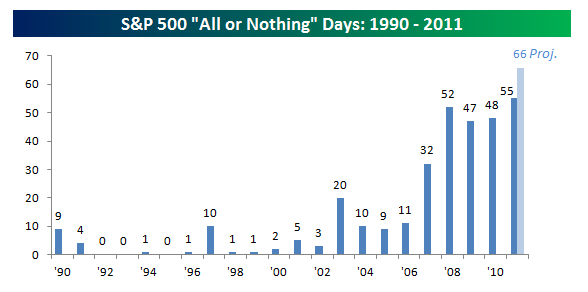

“We consider all-or-nothing days in the market to be days where the net daily [advance/decline] reading in the S&P 500 exceeds plus or minus 400,” Bespoke said. “There have now been 55 all-or-nothing days for the S&P 500 in 2011.”

Bespoke expects to see 66 total all-or-nothing days by year-end, compared to the 52 for all of 2008. Since the start of August, the markets have experienced 35 all-or-nothing days, which is more than the total from 1990 through 2001. [Stock ETFs See Extreme Advance/Decline Ratios]

Graphic source: Bespoke Investment Group

{kind=link}

For more information on the broader markets, visit our S&P 500 category.

Max Chen contributed to this article.