Major U.S. stock averages finished their worst Thanksgiving week in recent memory by extending their losing streak to seven sessions on Friday.

After challenging its 200 day moving average repeatedly in late October through the early part of this month, the S&P 500 finished Friday having lost about 9% from its recent highs and plunged through its 50 day moving average earlier this week without recovery. Friday was a rather volatile session although an abbreviated one with the early market close, as the futures improved quickly from premarket weakness to rise to the 1172 level in the SPX at one point, only to close with a whimper at 1158.67, and down on the session for the seventh straight day.

From a flows standpoint in exchange traded funds, risk aversion seems to be taking place which is certainly a change of pace from the activity that we have noted in recaps over the past several weeks. A number of fixed income related ETFs saw steady inflows during the week, including the likes of IEF, BIL, CSJ, MINT, and SHY, with the takeaway being that these ETFs track mostly short to medium duration U.S. Treasury securities.

Despite the very low, and to some, unappealing yields in U.S. Treasuries, it is apparent that investment managers are still flocking to fixed income based ETFs in times of market distress as way to simply “avoid” losing in equities or other asset classes that have simply not performed well recently.

More evidence of the “risk off” trades that occurred last week can be found in redemption activity, as we saw outflows in many of the broad market equity based funds such as SPY, IWM, QQQ, and DIA, with collectively more than $7 billion flowing out of those funds.

Additionally, one of the weakest sectors in the S&P 500 on a relative basis, XLF (which is down 9.59% in the past 1 month period with the S&P 500 down 5.25%), continued to fall this week, and put buying was evident in nearly every single session.

With the “one way” tape this week, the VIX was rather stagnant and traded in a fairly tight range in the $31-$36 level as it feels that market participants are not necessarily betting on a large move one way or the other in the marketplace going into to end of 2011. There has not been much in pivotal VIX options trading recently either, however trades that have taken place in recent weeks have mostly involved upside call buyers in the VIX, likely establishing “volatility hedges” going into year’s end.

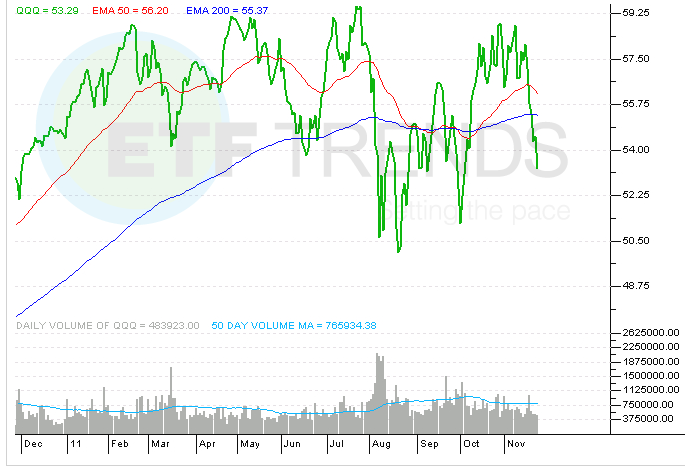

Of particular interest to us this past week was the precipitous drop in technology names, as the QQQ, after spending several weeks above both its 200 and 50 day moving averages, cratered to recent lows. This has been driven largely by severe weakness in QQQ top weighting, AAPL, which closed on friday right around its 200 day moving average ($363.90), and the stock has not spent much time at these levels since the August/September timeframe (although it did briefly trade lower momentarily in early October).

Heading into Friday’s action we also saw heavy put buying in SOXX, which would provide more evidence that fund managers are concerned with continued weakness in the tech sector over the next month or so heading into year’s end. Top components in SOXX include tech belwethers such as INTC, TXN, and AMAT. [ETF Chart of the Day: Semiconductors]

From a macro standpoint, the euro was under notable pressure this week, and the U.S.dollar rallied on the other hand, as FXE closed at its lowest levels since early October, and UUP vaulted accordingly. There has been consistent put buying in FXE as well as call buying in EUO in recent sessions, as it feels that institutional players have been “piling on” to a “short euro/long U.S. dollar trade” which is quite the opposite trade that was put on during the early part of 2011. We will see if the currencies experience a “whipsaw” as the last time the euro approached the $1.31 level against the U.S. dollar, it reversed course sharply and severely.

Next week, as trading volumes are likely to return to the market to some extent following the abbreviated Thanksgiving work week, we will be especially vigilant of recent cautious flows in the markets, and see if there is more bloodletting in store or perhaps a relief rally may surface.

PowerShares QQQ

For more information on Street One ETF research and ETF trade execution/liquidity services, contact pweisbruch@streetonefinancial.com.

{kind=link}