One of the main points in my prediction for a melt-up in stocks this fall was the lack of a catalyst or trigger. [Fall Melt-Up Arrives]

What I mean by this is that markets internally have behaved like a Lehman-like event has already happened, when in reality it has not.

Looking at the price ratios of defensive sectors (utilities, healthcare, and consumer staples) relative to the S&P 500 clearly shows that we hit levels not seen since the credit seize-up post 2008 crash, even though there has been no such situation (yet).

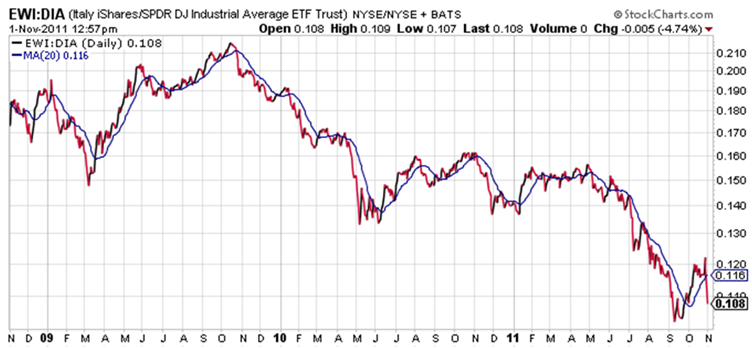

With Italy now looking vulnerable once again in the credit markets, I wanted to put a spotlight on the relative performance of iShares MSCI Italy (NYSEArca: EWI) versus SPDR Dow Jones Industrial Average (NYSEArca: DIA). As a reminder, a rising price ratio means the numerator/EWI is outperforming (up more/down less) the denominator/DIA.

{kind=link}

A few things worth noting in the chart above.

First, Italy has been underperforming the U.S. since mid-October 2009, and has been in a fairly strong and consistent period of underperformance since then. The decline especially picked up speed starting around June of this year, and bottomed out in September (before the historic move up in equities occurred in October). With news of the Greece referendum once again scaring market participants, the ratio took a sharp nosedive lower. However, this does not mean that outperformance is over.

Rather, the sharp pullback may be nearing its end right around these ratio levels, as the country potentially resumes its outperformance following the referendum in Greece.

Should the pullback be temporary and that ratio leadership persist, animal spirits likely would rise again and manifest themselves through risk-taking and stock buying. After all, wouldn’t an outperforming problem country index be bullish for worldwide equities?

The author, Pension Partners, LLC, and/or its clients may hold positions in securities mentioned in this article at time of writing. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities.