Bullish advisors have been telling investors to buy stocks because price-to-earnings multiples are historically low, making stocks cheap and attractive. At the same time, in bonds, Treasury yields remain depressed in a low-interest-rate environment.

For example, the S&P 500 is trading at 13.2 times reported earnings, compared to its average of 16.4 since 1954, according to a recent report. [Why the Stock ETF Rally May Have Legs]

Hopes for a year-end surge in U.S. stocks are rising after a sharp bounce in October, and many portfolio managers remain underinvested. [Equity ETFs Stumble Into November After Historic Rally]

Current valuations in stocks are “attractive,” said Doug Kass at Seabreeze Partners Management, in a RealMoney report Monday.

“Risk premiums (the earnings yield less the risk-free rate of return) stand at a multi-decade high, placing stocks, in theory, even cheaper than at the March 2009 bottom,” Kass wrote. “Looking out longer term in history, over the past 50 years the S&P 500 has averaged a 15.2x P/E multiple while the yield on the 10-year U.S. note averaged 6.67%. Today, the S&P 500 trades at only 12.5x (2012 earnings) while the yield on the 10-year U.S. note stands at only 2.05%.”

However, the mantra that “Stocks are cheap” has lost its power to persuade, “stifled by macro concerns that range from the arcane rules of Greek parliamentary process to the Borgia-esque machinations of the Italian political system,” says Nicholas Colas, chief market strategist at ConvergEx Group. “Or that of the U.S. Congress, for that matter.”

With investors fixated on the European debt crisis and the U.S. deficit, fundamental drivers such as P/E ratios appear to be less important to the market.

“’Stocks are cheap based on expected earnings’ carries about as much resonance as ‘put your baby tooth under your pillow and the tooth fairy will leave you a shiny quarter,’” Colas wrote in a recent research note.

With the S&P 500 hovering around 1,250, stocks are trading at 13.2 trailing four quarter earnings of $94.75.

“There is no actual ‘provable’ price-earnings multiple that investors can use to definitively state that this is X% cheap (or expensive),” the strategist said. “All those historical analyses you see rolled out are useless, because they almost always ignore interest rates.”

With rates very low by historical standards, it is hard to argue that a 13x multiple looks to be on the “cheap” end of the spectrum, he added.

“That said, U.S. stocks have been migrating to ‘cheap’ territory for a long time. The S&P 500 trading at 1,250 puts the index squarely in the middle of a very long term trading band,” the strategist noted. “Stocks may look cheap, but that is a trend that has been going on for half a generation and seems to lack a clear terminus. We need to ask ‘What will make them less cheap?’”

There are three answers to the question, he said: equities showing sustainable earnings power in another full-on financial crisis, progress on the U.S. budget deficit and a pickup in the U.S. employment market.

A bullish stance on U.S. stocks “needs to incorporate at least some of these scenarios to hold any real validity.”

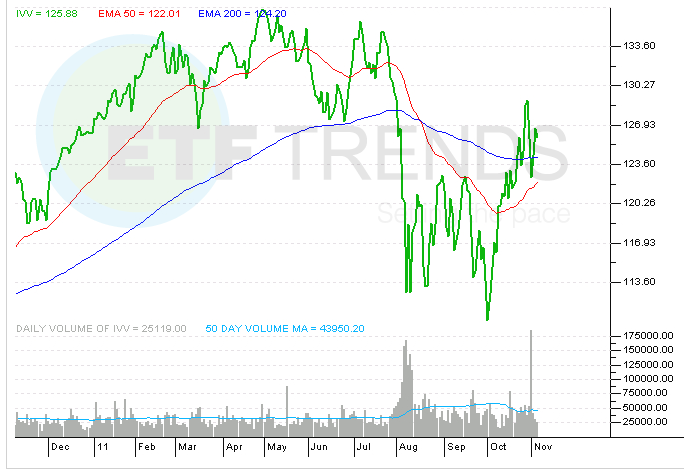

iShares S&P 500 (NYSEArca: IVV)

{kind=link}