As the equity markets have rallied sharply from lows touched on Tuesday of last week, the CBOE Volatility Index (VIX) has declined in seven of the past eight sessions, falling 33% from its recent high of 46.88.

We find the sudden decline in the VIX notable because the index is flirting with levels that were previously touched on three occasions since the sudden and vicious equity market selloff that began in early August. The VIX traded at 30.81, 30.16 and 30.43 on three separate occasions between August and today before resuming its uptrend.

It remains to be seen if the VIX breaks through 30 and stays there this time around, and in recent sessions we have seen evidence of institutional options players betting that this will happen. [Dow ETF Rallies; VIX Plummets]

Buyers of November and January 25 strike puts have been present in VIX options, and are speculating that the index will decline in the near term. This trading also expresses the sentiment of a “risk on” scenario where investors will likely be more comfortable with a sustainable equity market rally in the near term, so in short VIX put buyers should be bullish for equity returns if this trading is indeed directionally correct.

We also point out another dynamic in the VIX itself that likely is passed over by most market participants. There have been many critics of exchange traded funds and notes indexed to VIX futures in recent years because the VIX itself was mired in contango (meaning that distant month futures were priced higher than front month futures, and thus as the funds “rolled” positions forward, losses were immediately realized which hurt longer term returns). [Volatility ETF Critics]

This said, since the early August equity market selloff, the VIX migrated from contango into a state of backwardation (distant month futures priced below front month futures, and thus the “roll” is positive for returns) as investors largely

panicked and purchased portfolio protection via equity and index puts and volatility hedges via VIX options in a wholesale manner.

After the past few days of market action, the VIX futures curve is again approaching contango, as yesterday it was hovering literally tick by tick between contango and backwardation.

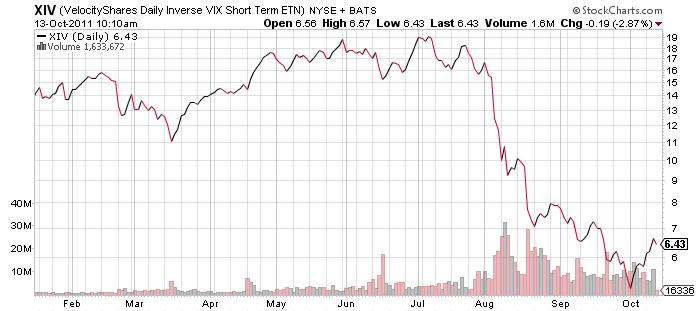

For those portfolio managers whom hope to bet against the VIX without using options, VelocityShares Daily Inverse VIX Short Term ETN (NYSEArca: XIV) may be an interesting play.

The fund has rallied considerably from an intraday low of $4.91 a share touched last Tuesday, and volume on Wednesday was above average.

It is important for the manager to understand the effects of the daily inverse objectives of the fund, as well as limitations and opportunities of the fund to track its objective based on whether the VIX itself is in contango or backwardation.

We do however expect to see a pickup in activity in XIV as well as other VIX related products as volatility itself continues to be in play from a speculation and trading standpoint.

VelocityShares Daily Inverse VIX Short Term ETN (NYSEArca: XIV)

{kind=link}

Chart source: StockCharts.com.

For more information on Street One ETF research and ETF trade execution/liquidity services, contact pweisbruch@streetonefinancial.com.