A couple months ago I started noticing significant distortions between and among sectors and various asset classes.

As a result, in early June I started penning articles warning that a stock crash was in the cards this summer. [Summer Crash of 2011?]

Make no mistake — we have experienced a crash in stocks. But we don’t know if it’s truly over or not.

The crash of 1987 took the Dow Jones Industrial Average back to levels not seen since nine months prior. The summer crash of 2011 has taken the S&P 500 to levels not seen in 10 months.

There are two important sectors now to pay attention to. Since the March low in 2009, the main drivers of the equity bull market were industrials and consumer discretionary. They significantly outperformed broader averages since the liquidity-induced recovery began.

However, a break in leadership in industrials and early shift out of discretionary stocks appears to be occurring. Below are the price ratios comparing the industrials and consumer discretionary sectors to the broader market. As a reminder, a rising price ratio means the numerator/sector is outperforming (up more/down less) the denominator/S&P 500.

Industrials — Don’t Cry for Me

{kind=link}

Industrials fell off a relative cliff starting in July, effectively giving up all of its alpha/outperformance attained since early 2010.

The swift loss of leadership was an early tell that not all was well with markets.

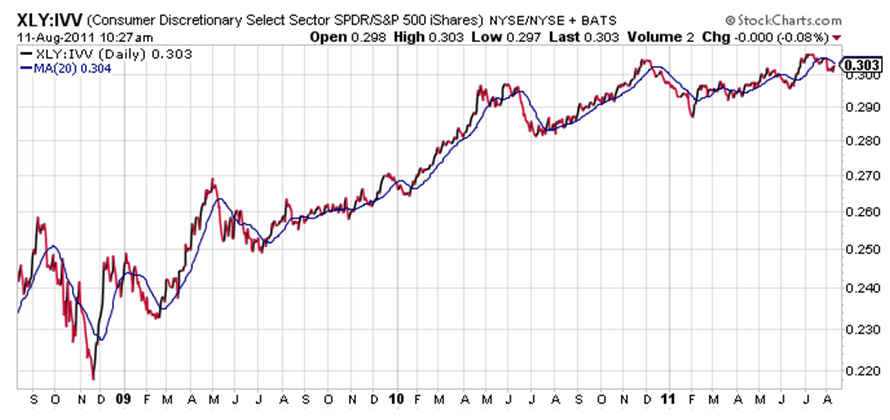

Consumer Discretionary — Going Down Swinging

{kind=link}

While consumer discretionary has not declined as substantially relative to the market as industrials, I believe leadership is on the verge of ending in a major way.

Notice that the discretionary sector bottomed out mid-November 2008, providing an early signal that markets were on the verge of bottoming before the March lows.

The bottom line is that while industrials and consumer discretionary were market leaders, these two sectors remain vulnerable from an outperformance standpoint regardless of whether markets have bottomed following the summer crash of 2011.