S&P 500 exchange traded funds rallied nearly 3% on Monday following a report that U.S. stocks haven’t been this cheap since Ronald Reagan was in the White House.

The U.S. blue-chip stock index has plummeted 13% over the last five weeks, with the average price-to-earnings ratio down to 12.9, a level not seen since Reagan was in office back in 1982, reports Inyoung Hwang for Bloomberg. [ETFs Rally on ‘Attractive’ Valuations, Fed Hopes]

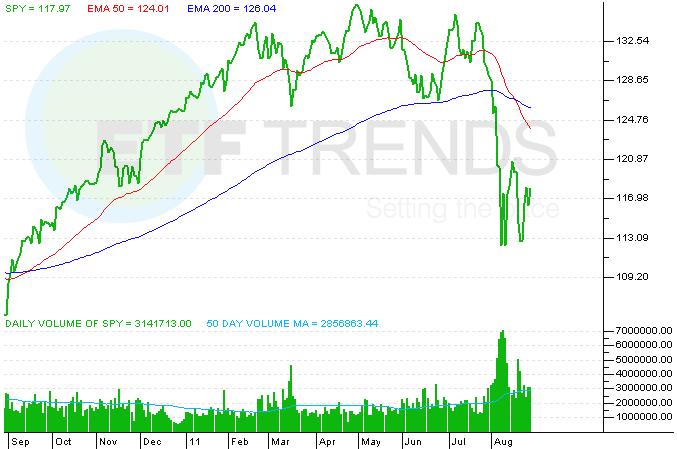

The U.S. stock market has seen its value decline by over $2 trillion in the recent sell-off after the S&P 500’s recent high in late July, according to the report.

Bearish observers believe that the U.S. has been stuck in a slowdown since 2007, arguing that with interest rates already near zero, the Federal Reserve has become limited in its ability to combat the recession. On the other hand, bullish observers point out that skittish investors, fearing another possible repeat of 2008, are trading extremely pessimistically.

“There are truly some terrific values out there in companies, but it’s a question of timing,” remarked John Massey, a fund manager at SunAmerica Asset Management, in the Bloomberg report. “Right now, the market is very short-term sighted. Every day the market is up or down, and it’s much more of a macro call than anything else.” [Are ETFs Causing Correlation Spike?]

According to Bloomberg, the S&P 500 traded at 10.8 times forecasts for profits over the next 12 months of $109.12 a share at the end of last week. In contrast, earnings would have to fall to $71.76 a share if the P/E ratio were to rise back to its 50-year average of 16.4 without appreciation in share prices.

However, TCW Group Inc.’s Komal Sri-Kumar believes that valuations need to keep dropping before prices are justifiable in a stagnating economy.

“Stocks have been at very high levels compared with a very weak economy,” commented Sri-Kumar, the chief global strategist at TCW. “When QE2 was introduced last August, you got a rally in equities prices for several months, but you didn’t get a big push up in economic growth.”

Other analysts point out that analysts’ profit forecasts may be too high. “Also unsaid was the impact of recession on earnings,” Barry Ritholtz, chief executive at quantitative research firm Fusion IQ, commented on the Bloomberg report.

“The Reagan Recession came at the end of a 16-year bear market, plus benefited from [Federal Reserve Chairman Paul Volcker] breaking the back of inflation. The threat today is a Japan-like deflationary spiral, including falling asset prices and an unwillingness for investors to buy up for a dollar of earnings,” Ritholtz wrote. “In other words, a falling [price-to-earnings ratio] could be evidence of an ongoing deflationary phase, and not proof that markets are cheap.”

SPDR S&P 500 ETF (NYSEArca: SPY)

{kind=link}

Max Chen contributed to this article.

Full disclosure: Tom Lydon’s clients own SPY.