For financial advisors, municipal bond exchange traded funds (ETFs) have been a boon and a burden at the same time.

{kind=link}

The plus side is that the new muni ETFs provide a safer, lower cost way of investing in municipal bonds than either municipal bond mutual funds or direct investments. The bad news? Today’s investment climate is so crazy that market watchers warn that the muni market could be rough this year.

As an investment vehicle, muni ETFs have a lot going for them. Generally, fees are about half of a municipal bond fund-0.20% to 0.40%, compared to 0.50% to 0.80%. Right now, even if it’s just half a percent you’re saving, that’s a lot of money.

Muni ETFs are also more transparent than most bond funds, which only have to report what they held last quarter. They’re slightly more liquid, too. Unlike mutual funds, which can only be sold at the net asset value of the prior day’s closing price, muni ETFs can be sold at the prevailing price any time during the day.

There’s not been a hiccup as far as trading, the spreads have been very reasonable and manageable, reports On Wall Street.

On the plus side, yields are high right now relative to U.S. Treasuries. In ordinary times, municipals trade at yields a little lower than Treasuries, pricing in their tax advantages.

Munis are also tax-free, of course, and double-tax free if your client is a New Yorker or Californian who buys a home-state muni ETF. Defaults can happen, but are rare, at least compared to corporates. The major downside to the muni market is that since the insurance is not available, institutional investors steer clear of this investment class. Both leveraged investors and individuals are not interested in munis either.

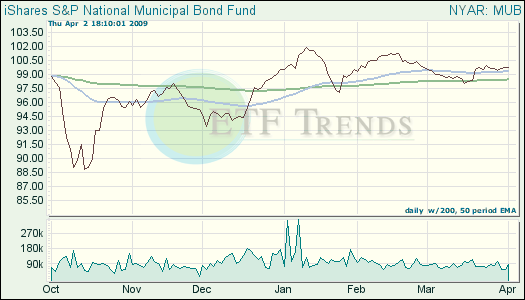

To cope with the downside risk of a muni ETF, keep your eye on the 200-day moving average, and if the fund falls below this, it may be time to get out.

- iShares S&P National Municipal Bond ETF (MUB): up 1.2% year-to-date; up 0.4% for one week; 3.55% yield

{kind=link}