By Rod Smyth, RiverFront Investment Group Chief Investment Strategist

2017 presents markets with significant potential policy changes on taxation, regulation, healthcare, infrastructure and trade. After years of gridlock, where the main focus of policy has been on central banks, now the focus is squarely on the new administration and Congress. On balance, we expect global stocks and interest rates to rise.

Since November, the prevailing mood of investors has been one of optimism about faster economic earnings growth from lower taxes and less regulation, and we agree. For now, the more alarming rhetoric on trade seems to have been viewed as part of a negotiation. At RiverFront, we recognize that policy negotiation through tweeting is just a part of the new world. Our challenge is to avoid the emotional cycle generated by the headlines and seek to assess policy changes that we believe will actually occur. For now, we will seek to make changes when we believe assets become mispriced. The baton pass from the dry language of central banks to the colorful one of politicians is our new reality.

One example is corporate tax reform. There is clear commitment from the President and from the Republicans in Congress to lower corporate taxes. There does not seem to be a big divide on the rate: the House of Representatives’ plan suggests 20%, President Trump has indicated he would prefer 15%, and both are lower than the current 35% rate. If implemented, however, the House plan proposes a fairly radical change in how taxes are assessed. Currently taxes are levied on the difference between worldwide (total) income and worldwide (total) costs.

The proposed plan, as we understand it in simple terms, would tax only the difference between domestic revenues and domestic costs. Thus, overseas revenues would not be taxed, but a company whose revenues were all in the US and whose costs were all from imports, would have no costs to deduct and therefore pay tax on all of its revenues. Thus, although overall tax rates would come down, different business models would be impacted very differently. This concept is becoming known as a “border tax adjustment”.

The House’s blueprint is just the beginning of a negotiation. President Trump has tweeted that the plan is too complicated, and the Senate has yet to really get involved. The making of policy is usually complicated and messy. We will seek to assess the impact when a clearer consensus emerges. We think this will take months and involve plenty of public debate, but we do expect corporate taxes to be cut in 2017, potentially retroactively.

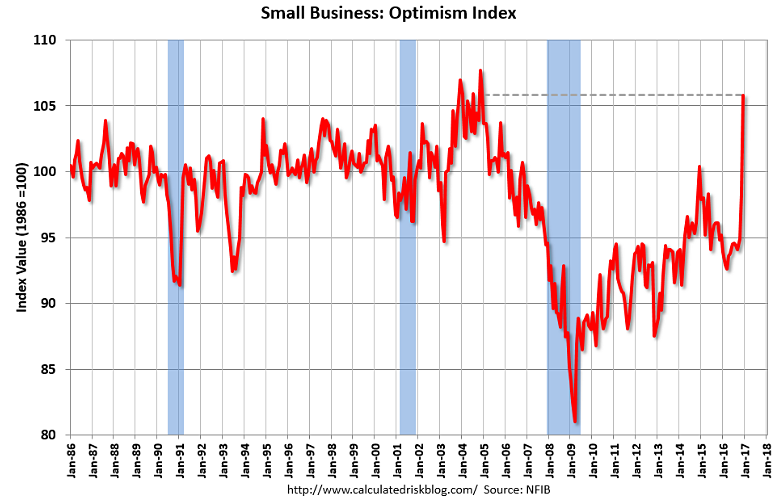

We also will continue to focus on the data, and one piece of recent data we find striking is the rise in small business optimism. As you can see from the chart on the next page, courtesy of calculatedriskblog.com, the latest surge in optimism as reported by the National Federation of Independent Businesses (NFIB) is pretty exceptional by historic standards and takes the index back to levels last seen in 2004/2005. Small businesses potentially stand to benefit from tax cuts, both corporate and personal, and from a more business friendly regulatory environment, in our view.

THE WEEKLY CHART: SMALL BUSINESS OPTIMISM SURGES

Source: http://www.calculatedriskblog.com. Chart published on January 10, 2017.

Notable within the survey was the response to the question as to whether the businesses “expect better business conditions”. In that category, the respondents went from 12% in November to 50% in December. We believe this indicates that small businesses are building up their expectations of what the new administration is going to do for them. In the short term, business confidence can be self-fulfilling, which we think should keep the employment market healthy and the Fed on track for gradual rate hikes. As the year progresses, we think that both businesses and investors will need to see concrete proposals and ultimately legislation in order to maintain this momentum.

We expect legislation to lower corporate tax levels, but as stated above, we do not yet have clarity on what that will look like. We also predict that the benefits will probably be greater for smaller businesses that typically pay higher taxes than large multinationals, because the latter can take advantage of different tax regimes around the world.

Important Disclosure Information:

Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past. Diversification does not ensure a profit or protect against a loss.

RiverFront’s Price Matters® discipline compares inflation-adjusted current prices relative to their long-term trend to help identify extremes in valuation.

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Strategies seeking higher returns generally have a greater allocation to equities. These strategies also carry higher risks and are subject to a greater degree of market volatility.

RiverFront Investment Group, LLC, is an investment adviser registered with the Securities Exchange Commission under the Investment Advisers Act of 1940. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). RiverFront also serves as sub-advisor to a series of mutual funds and ETFs. Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations. Copyright ©2017 RiverFront Investment Group. All rights reserved.