Note: This article is part of the ETF Strategist Channel on ETF Trends.

By Rod Smyth

The son of a good friend of mine, a successful millennial in San Francisco, is getting married, and we were discussing the viability of buying a 1,000 square-foot apartment. The price – $1,000,000.

To my surprise, putting aside the challenges of anyone that age paying a million dollars for a small place to live, the economics of buying an apartment in a city with such a high cost of living appear to be reasonable.

If he goes ahead with the purchase, he will pay little more per month on a 30-year fixed mortgage than he is currently paying in rent, and it will be going towards building equity. That passes a reasonableness test that few property markets were able to pass in the mid 2000’s, but many do today.

The math works because of high rental levels in San Francisco and low long-term mortgage rates. The risk is that a price decline wipes out his down payment (due to a recession in the technology industry for example). That is a risk anytime one purchases a home.

Last year in a Weekly View dated May 26, 2015, we argued that while millennials have different living preferences, we believed that once they settled down they would prefer to own than rent. Household formation started to accelerate in 2015 and continues to do so as the job market improves and millennials / Gen-Xers get older. Like previous generations, it would appear that they are switching from renters to buyers. We believe these trends have a long way to go, and thus we remain optimistic on the housing sector.

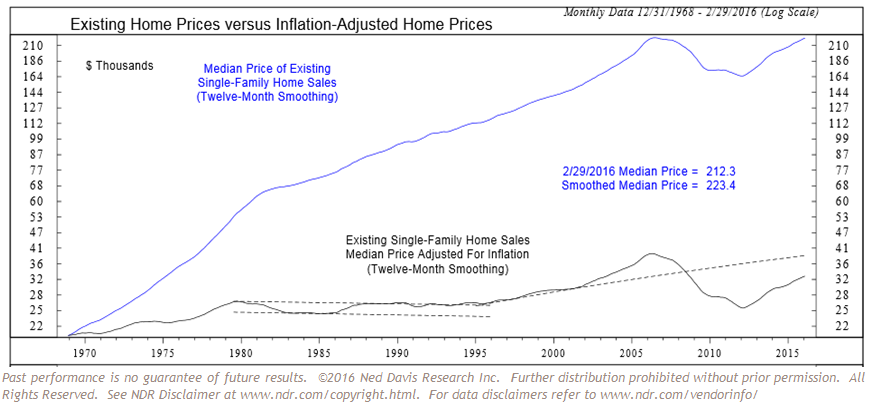

{kind=link}

The above chart shows that since 1969, the median price of a single family home has risen roughly 10 times, or about 5% a year. Adjusted for inflation, a one-year smoothed price has risen just 65% over the whole period. Home prices have recovered their 2007 peak after nine years (another lost decade), but not so after inflation where they remain little changed over the last 15 years. With interest rates so low, we believe that single family homes look like a fairly priced investment and are a potential hedge against inflation.

Our view that 2016 will be a year of higher stock prices and no recession is supported by economic data.

While it is rarely as simple as one thing, we believe that the correction in risk assets during the first quarter was substantially driven by a growing fear that slower economic growth would lead to a recession. Indeed, credit spreads, the difference between the yield on corporate bonds (investment grade and high yield), went to levels usually only seen heading into recessions. We maintained throughout the first quarter that markets were worrying too much about the sustainability of the current global expansion. In the dark days of February, it might have seemed hard to believe that the S&P 500 would finish the quarter virtually unchanged.

We believe the main driver of the rally off the February lows has been data that has been strong enough to support stocks, but not so strong as to raise fears of a significant tightening cycle by the Fed. We think the rest of the year, while potentially volatile, will see higher stock prices as slow growth continues. This view is supported by Friday’s Nonfarm Payroll data, which suggested the economy added another 215,000 jobs. The Weekly Chart below shows that the current expansion, while slow, has added some 10 million jobs, which we believe is significant. New workers came into the workforce in March, and average hourly earnings grew at an annualized rate of over 3%. A prolonged cycle that is slow and steady is exactly the right remedy for a balance sheet led recession as it has allowed corporate and personal balance sheets to improve, and makes the government’s debt payments affordable. We remain strategic bulls of risk assets. Accordingly, our risk management and tactical team recently brought risk levels in our portfolios back in line with our strategic targets.