Q4: Jodie, despite difficult returns this year, we’ve seen a mini-revival in commodity investing by pension funds and growing interest by individual investors. What are some of the reasons for this and do we expect this trend to continue next year? The main reasons investors are turning to commodities are the same as throughout history, which are diversification and inflation protection with the potential of equity-like risk and returns. Although these reasons hold in the long run, many investors questioned the true diversification commodities provide since they fell in the financial crisis with each other and the other asset classes. The risk-on/risk-off environment has proved difficult for commodities, especially as portfolio diversifiers to protect capital. Today, there are new factors overtaking the risk-on/risk-off environment that are bringing down correlations to pre-crisis levels, which you can read more about here:

As suppliers have reduced production post-financial crisis and inventories have been reduced, finally the supply shocks, are driving commodity returns again and cause them to be different from each other and from equities and fixed income. This is creating the most opportunity for spread plays and diversification since 2007.

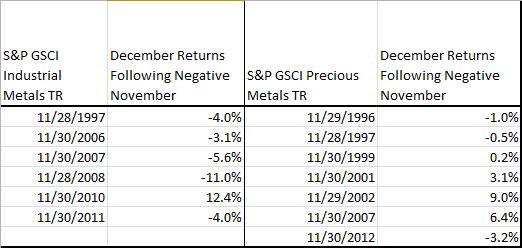

Bonus question: Will metals continue their downfall? The interesting thing about metals is the difference between the industrials and the precious metals. Since 1995, there were 6 Novembers where industrial metals had negative returns and 5 out of those 6 times there was a negative December following. This is not surprising given the sensitivity of industrial metals to the inventory situations. Given the more difficult storage situations of some industrials like copper, it may be difficult for suppliers to meet the demand so the equilibrium is balanced by price, causing a persistent trend. [The possible reason for the persistence in realized roll yield may be, as discussed in Till and Eagleeye (2005), “if there are inadequate inventories for a commodity, only its price can respond to equilibrate supply and demand, given that in the short run, new supplies of physical commodities cannot be mined, grown, and/or drilled. When there is a supply/usage imbalance in a commodity market, its price trend may be persistent….“ ]

On the other hand, precious metals, which are well supplied and easy to store, have had 7 negative Novembers but only 3 of the following Decembers were down.

Source: S&P Dow Jones Indices. Data from Jan 1995 to Nov 2013. Past performance is not an indication of future results. This chart reflects hypothetical historical performance. Please see the Performance Disclosure at the end of this document for more information regarding the inherent limitations associated with backtested performance

Different fundamentals that are more aligned with their “store of value” qualities like central bank buying and flight to safety, drive the precious metals. Since the precious metals are largely abundant, there is less trending from price as the calibrating factor to balance supply and demand. Overall, it is not surprising that in all calendar months over the time span Jan 1995-Nov 2013, that industrial metals moved in the same direction as in the prior month 51% of the time, but precious metals only moved in the same direction as in the prior month 46% of the time.

About Jodie Gunzberg

Jodie M. Gunzberg is vice president at S&P Dow Jones Indices. Jodie is responsible for the product management of S&P DJI Commodity Indices, which include the S&P GSCI® and DJ-UBS Commodities Index, the most widely recognized commodity benchmarks in the world. Both indices represent the global commodity market and are most commonly used for the historical benefits of inflation protection and diversification to stocks and bonds.

© S&P Dow Jones Indices LLC 2013. Indexology® is a trademark of S&P Dow Jones Indices LLC (SPDJI). S&P® is a trademark of Standard & Poor’s Financial Services LLC and Dow Jones® is a trademark of Dow Jones Trademark Holdings LLC, and those marks have been licensed to SPDJI. This material is reproduced with the prior written consent of SPDJI. For more information on SPDJI, visit http://www.spdji.com.