Obviously, if the trend for bonds were to continue unabated, a buy-n-holder of bond assets might be cruising for a bruising.Yet how likely is the trend to continue unabated? How likely is it for the Federal Reserve to taper or slow or tighten in future months when inflation is lower than targeted and wage deflation is dragging on the economy? How likely is it for the Fed to do much more than “save some face” in mid-September when they meet, when real estate is highly dependent on the manipulated rate structure that they’ve set up? And how likely is it for institutional money to completely abandon an entire asset class after the 140 basis point surge? From where I sit… not bloody likely.

So when will bond investments turn around? Well, the debt ceiling debacle did it back in 2011… but I wouldn’t count on a drawn-out debate this time. More likely, bonds will be back in favor when the investment community interprets genuine commitment to keep intermediate-term rates from climbing beyond its reach. And to be frank, if bonds were able to hold steady, the cash flow alone might be a worthwhile reason to maintain some exposure. In essence, yield-hungry folks would be able to generate better income streams from”safer” harbor investments.

Let’s not forget another reason to own fixed income. Bond ETFs can reduce overall portfolio volatility. So while it may seem that the 2-year stock rally is the only thing worthy of notice, and the 2-year 0% return for most bond holdings are unsavory, the next stock market correction of 10%-20% would change those figures in a heartbeat.

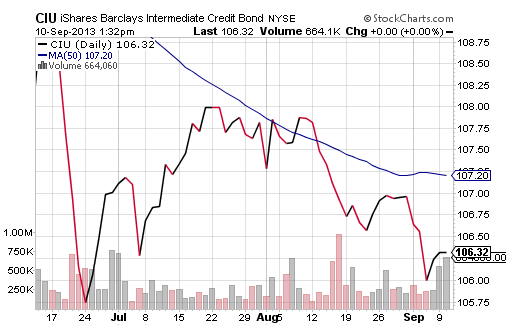

At this time, though, my client portfolios do not happen to have much in the way of treasury debt. My largest income holdings include PIMCO Short-Term High Yield (HYS), PowerShares Senior Loan (BKLN), iShares 1-3 Year Corporate (CSJ) and iShares Intermediate Corporate (CIU). The latter has been hit the hardest by the spike in the 10-year Treasury. However, if the June lows for CIU hold, the 3% annualized cash flow delivered monthly could be augmented by a modest amount of price appreciation on a “Sell the Rumor, Buy the News” Fed tapering event.

{kind=link}

Gary Gordon is president of Pacific Park Financial, Inc.