In this installment of our Retirement 101 blog series, we’ll discuss how to afford saving for retirement even when times are tough.

When the economy goes south, people often forget about retirement planning or just stop doing it because they think they can’t afford it. But the truth is that you can’t afford not to save for retirement.

Costs only go up over time, and the longer you put off saving for retirement, the harder it will be. It’s never too late to start saving for retirement, but the earlier you start, the better off you will be. Remember that, while you can finance things like college, homes, weddings, etc., you cannot finance your retirement. You have to pay for it yourself. And regardless of how economically you live, Social Security will likely not be enough to cover your needs.

So how can you afford it right now?

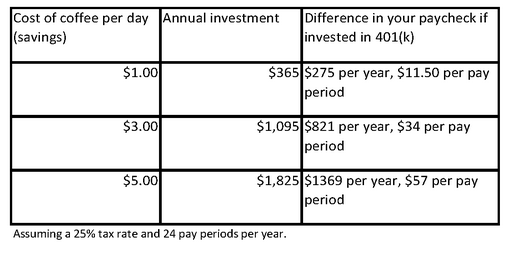

You may be wondering how to afford it when you’re already struggling to make ends meet. But it may be easier than you think to make a small sacrifice now that can add up to a big difference later. For example, how much is that cup of coffee you grab every day? Maybe you think that saving that $1 a day won’t make a big difference over time, but it could. [WisdomTree: The Importance of Keeping Your 401(k) Invested]

One dollar per day is more than $300 per year, $3 per day adds up to nearly $1100 per year, and $5 per day is more than $1800 per year. Over time, that $300, $1100 or $1800 you invest can begin to compound and create a really significant difference in your retirement readiness. Plus, if you invest that money in a tax-deferred 401(k) plan, that $300 feels more like $225 to you. Even $1800 feels closer to $100 a month or $50 per pay period. Again, that small sacrifice now could make a big impact later.

{kind=link}