U.S. equity markets have been roaring in 2013, with new market highs being set. In the face of such strong performance, whispers abound about the potential for a pullback.

The 2013 rally has been led by higher-dividend, defensive sectors, and we have seen some analysts question whether there is a “dividend bubble.”

To the contrary, we think dividend stocks in aggregate are attractively priced; below we discuss differences among segments of the dividend market and higher-dividend sectors.

Current Sector Valuations

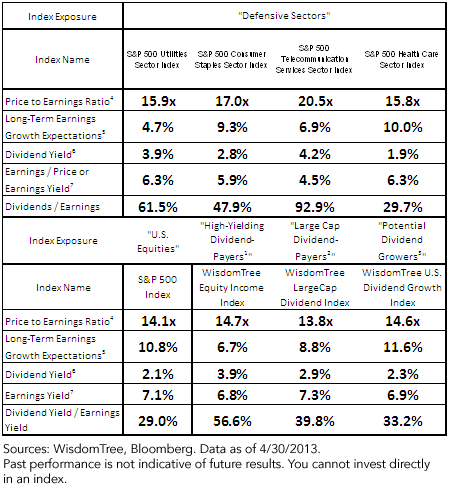

Looking at the S&P 500 Index (“U.S. equities”), the four sectors that have led the rally from the beginning of 2013 to the end of April have been Utilities (+19.74%), Health Care (+19.22%), Consumer Staples (+18.11%) and Telecommunication Services (+17.07%) (i.e., the “defensive sectors”).

Typically, firms in these sectors have relatively higher dividend yields.

Index Valuation Characteristics

{kind=link}

• Defensive Sector Price/Earnings (P/E) Ratios: U.S. equities, defined by the S&P 500—an index weighted by market capitalization that does not focus on dividends in any way—had a P/E ratio of slightly over 14x as of April 30, 2013. The four defensive, typically higher-dividend, sectors all had higher P/E ratios than that of broader U.S. equities, ranging from 15.8x to 20.5x. These numbers are why some analysts consider high-dividend stocks to be expensive.

• Long-Term Earnings Growth Expectations: Additionally, each of the defensive sectors has lower long-term earnings growth expectations, ranging from a low of 4.7% for Utilities to a high of 10.0% for Health Care.

• Dividend Yields: The dividend yields on these defensive sectors range from 1.9% for Health Care to 4.2% for Telecommunication Services.

• Dividend Yield / Earnings Yield: We find it interesting to compare the dividend yields of these indexes to their earnings yields in order to illustrate the impact of dividend policy. What we see is that the Telecommunication Services sector is paying out the vast majority of its earnings as dividends by this metric—that’s how it generates such a high yield. The Health Care sector is on the opposite end of the spectrum, paying out only about 30% of its earnings as dividends.

Next page: Misguided conclusion