One of the oft-cited “value propositions” of ETFs is that they are lower cost than traditional mutual funds. While this may be true when you use simple averages for all ETFs and all mutual funds, the opposite picture emerges when you asset-weight the averages, showing what investors are actually paying.

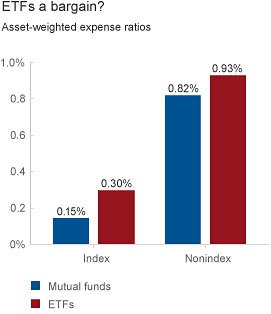

In fact, investors in index ETFs pay an expense ratio that is twic eas high as investors in traditional index mutual funds.

How is that possible? First, it’s important to understand that the vast majority of ETFs (97%) are indexed, while only 13% of traditional mutual funds are indexed (Morningstar, Inc., as of February 28, 2013).

The chart below separates index and active strategies and shows asset-weighted expenses (as a percentage of assets) paid by investors. ETFs, the supposed bastion of lower costs, are more costly in both categories—by significant margins.

{kind=link}

Source: Morningstar, Inc., as of February 28, 2013.

Given the pervasive marketing pitch about ETFs being lower cost than traditional mutual funds, this may be a surprise. There are a few reasons that help explain this result:

- Traditional mutual funds offer lower-cost share classes for accounts with larger minimum balances, bringing down the average.

- The index ETF category includes a larger proportion of assets in alternatively weighted index strategies, which generally charge higher fees than traditional indexing.

- The index ETF category also includes many strategies based on physical commodities, which are generally not available in traditional mutual funds and tend to charge higher fees.

The missing link: ETF sponsors’ profits paid by investors

Even so, I can hear the shouting now. “But … but … but … ETFs are lower cost than mutual funds because the sponsor doesn’t have to interact with thousands or millions of individual shareholders.” Or: “Traditional funds are lower simply because Vanguard, with its at-cost management structure, currently has a larger market share in index mutual funds than among ETFs.”