Uncertainty over the election outcome in Italy caused a broad-based sell-off in global equities—particularly Italian equities—as well as the euro.

Does this mean one should not invest in European equities in general? Many believe the relatively low prices of European stocks represent an attractive entry point, despite the political uncertainty and the relatively sluggish economies.

For those considering increasing their allocations to Europe, I wonder: Why bother taking the currency risk1 of the euro? Recent euro volatility serves as a fresh reminder that currency volatility can compound the volatility of European equities—for U.S.-based investors2.

One Way to Potentially Lower Risk of European Equities: Hedge the Euro Risk

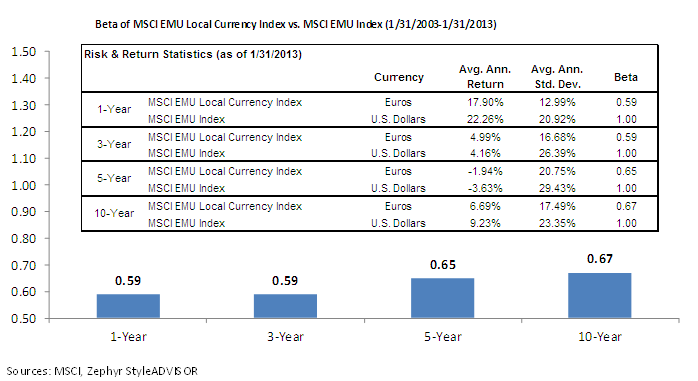

I looked at how much additional risk euro volatility has added to European equity indexes over all the major periods: 1-, 3-, 5- and 10-year periods (ending January 31). A few remarkable conclusions:

{kind=link}

(For definitions of terms in this chart, please see our Glossary.)

• Removing euro risk from the equation lowers the beta of the MSCI EMU Local Currency Index by 33%–35% over the 5- and 10-year periods and by over 40% over the 1- and 3-year periods ending January 31, 2013.

• The standard deviation, or risk, of the MSCI EMU Local Currency Index was just 12.99% over the last 1-year period, but the risk of the MSCI EMU Index exceeded last year’s by almost 21%.

• Even on a 10-year basis, volatility of the MSCI EMU Local Currency Index was lower (17.49%) than that of the MSCI EMU Index (23.35%).

One might counter that currency risk is worth it if it provides additional benefits in the form of higher expected returns. But I find no evidence that assuming currency risk has done any such thing. And why should it? There is no theoretical model I know of that would suggest the euro should always appreciate against the dollar. There will be times when euro exposure increases returns to European equities and times when euro weakness subtracts from returns for U.S. investors. What has tended to happen is that the euro’s fluctuations have created additional volatility for European equity indexes priced in dollars—as we saw in the major periods illustrated earlier.

I thus have been advocating that those who want to target European equities consider one of two strategies:

1) Hedge your euro exposure, as this can potentially lower the overall risk to European equities.

2) Consider a 50% euro hedged/50% euro unhedged exposure to help minimize your regret of being on the wrong side of a currency decision. I wrote about this 50/50 framework in an earlier blog.