While the resurgence of risk appetite over the past month has seen a rotation toward more cyclical assets, investor sentiment remains fragile, as evidenced by the market plunge following the Italian election results.

Prior to the announcement of the Italian election results, net speculative longs in metals with industrial uses such as platinum, palladium, silver and copper remained either close to or at their all-time highs, while major equity markets had posted solid gains.

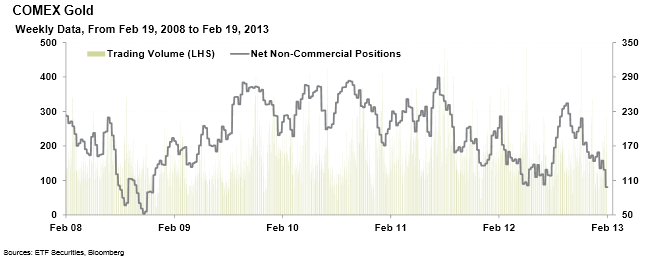

Gold fundamentals remain constructive

Meanwhile, net speculative longs in COMEX gold had hit the lowest levels since December 2008 (see chart), as investors seemed positioned for ‘the worst is over’ scenarios. How quickly sentiment can shift. The gold price came under pressure last week as some investors overreacted to the release of the January FOMC minutes, believing discussions about the timing of stimulus withdrawal would prompt a premature end to the Federal Reserve’s economic support.

A rebound in the gold price followed Fed Chairman Bernanke’s testimony to the House Financial Services Committee with investors appearing to revise their (mis)interpretation of the FOMC minutes. Bargain hunters have since begun to emerge, giving some stability to the gold price around US$1,600oz, while trading turnover on the Shanghai Gold Exchange hit a daily record last week.

While the technical picture fueled the liquidation of gold holdings and the subsequent price decline, macro fundamentals suggest a potentially attractive entry level, as global financial markets remain awash with liquidity, global interest rates expected to remain extremely low for the foreseeable future and key macro risks lingering, particularly for the Eurozone economy that is likely to remain in recession in 2013 according to the European Commission.

{kind=link}

Gold remains a hedge against downside risks to the cyclical recovery

The failure to avert the automatic spending cuts that will take place this week (March 1st) in the US is a cogent reminder that policy paralysis could stop the global recovery in its tracks. Starting with Italy, austerity-fatigue could lead to a change in policy course more generally across Europe, threatening investor sentiment that has taken so long to recover.

The inconclusive results from the Italian General Election have already rattled markets and could further weaken the Euro. Investors are likely to find increasing value in gold as a hedge against downside scenarios given that its price is now 16% below its peak reached in 2011 (in US Dollar terms).