With the Indian rupee coming off historic lows, we believe potential foreign direct investment could provide the necessary boost for further currency appreciation.

2011 and 2012 were not great years for the Indian rupee. Persistent concerns about inflation and a slowing global economy created an environment that policy makers and investors found very difficult to navigate.

However, 2013 is off to an encouraging start, with strong flows forcing the currency up from its historic lows reached in June 2012.

With moderating inflation giving it some flexibility to cut interest rates, and in an effort to revive growth, on January 29 the Reserve Bank of India (RBI) went ahead with a 0.25% rate cut for the first time since April of 2012.

While current foreign exchange forecasts are calling for only a moderate appreciation of 2.6%,1 the high levels of interest carry could be an attractive cushion for investors looking to make an allocation to one of the world’s largest and fastest-growing economies.

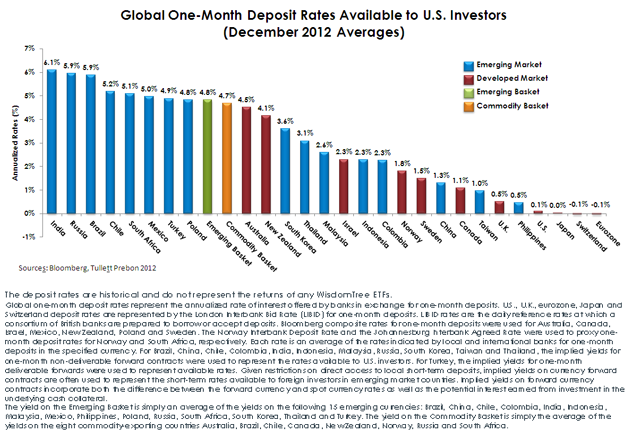

{kind=link}