In my past post on dividend-paying stocks, some responded with questions about REITs (real estate investment trusts). You asked whether REITs are effective “bond substitutes,” whether they are a “defensive” equity investment, whether they’re good short-term hedges against inflation, and about their recent outperformance versus the broader stock market.

My answers are “No,” “not recently,” “no,” and “be cautious.”

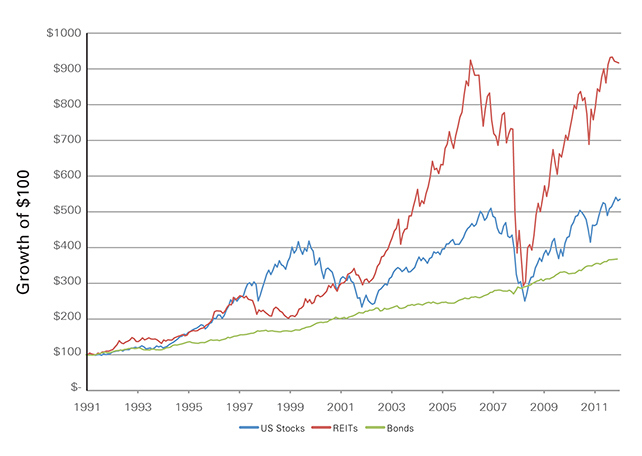

With current yields on broad fixed-income portfolios less than appealing to many investors, some have argued the merits of substituting dividend-paying stocks—and REITs, in particular—for bonds. They base their argument on the fact that current bond yields are lower than the dividend yield for REITs—1.7% for the Barclays U.S. Aggregate Index versus 3.4% for the FTSE NAREIT All Equity REITs Index—and that the upside potential for stocks in any equity rally is higher than for bonds. However, as you’ll see in the chart below, REITs tend to correlate with the broader equity market, not with bonds. This is especially true in down stock markets, such as 2008-2009. [Global Real Estate ETF with 4% Yield]

At times, REITs may outperform the broader equity market (as they have over the past several years), and vice versa. But, as the chart illustrates, if you substitute REITs for bonds in order to generate greater income, the final result is a more aggressive and more stock-heavy strategic asset allocation. In doing so, we would expect an increased likelihood of higher nominal returns over long periods of time, but that’s not necessarily because of the higher anticipated income stream. Rather, it’s because stocks are riskier and more volatile than bonds.

While I certainly sympathize with investors struggling in this low-yield environment, I just hope that we all appreciate that dividend-paying stocks, including REITs, are not substitutes for bonds. That’s not to say they won’t outperform a broad bond portfolio over the next several years. Rather, my point is that such an income-focused strategy is not a no-brainer, nor is it risk-free.

{kind=link}

Sources: Vanguard calculations based on data from Dow Jones, MSCI, FTSE, and Barclays. U.S. stock returns represented by Dow Jones Wilshire 5000 from 1991 through April 2005 and MSCI U.S. Broad Market Index since May 2005; REITs returns represented by FTSE NAREIT All Equity REITs Index; and bond returns by Barclays U.S. Aggregate Bond Index.

REITs as an inflation hedge? It depends